ZETA: Q4'25 Earnings Review

Zeta Global Delivered Its 18th Consecutive Beat-and-Raise Quarter, Guides to GAAP Profitability in 2026.

Financial Results For FY2025

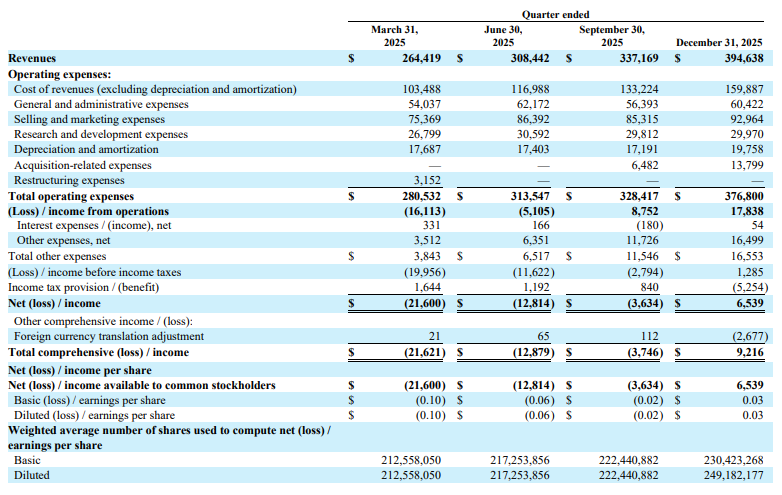

Revenue

Fourth quarter revenue of $394.6 million, up 25% Y/Y, exceeding the midpoint of guidance by $14 million

Organic growth of 28% Y/Y when excluding political candidate, LiveIntent, and Marigold’s Enterprise Business revenue

Full year 2025 revenue of $1.305 billion, up 30% Y/Y (27% on an organic basis)

16th consecutive quarter of greater than 20% revenue growth

Profitability

Q4 Adjusted EBITDA of $95.1 million, up 35% Y/Y, with margins expanding 174 bps to 24.1%

Full year Adjusted EBITDA of $278.7 million, up 44% Y/Y, with margins expanding 217 bps to 21.4%

20th consecutive quarter of expanding Adjusted EBITDA margins on a Y/Y basis

Achieved positive GAAP net income of $6.5 million in Q4, representing a 1.7% margin

Cash Flow

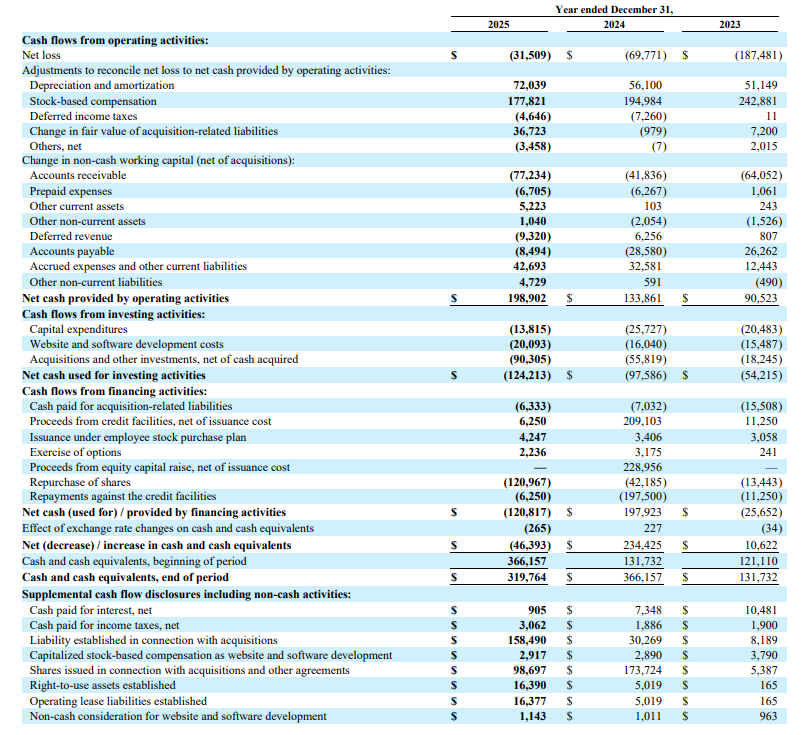

Full year operating cash flow of $198.9 million, up 49% Y/Y

Free cash flow of $164.7 million, up 78% Y/Y

FCF margin of 12.6%, up from 9.2% in FY2024

FCF to Adjusted EBITDA conversion of 59%

Customer Metrics

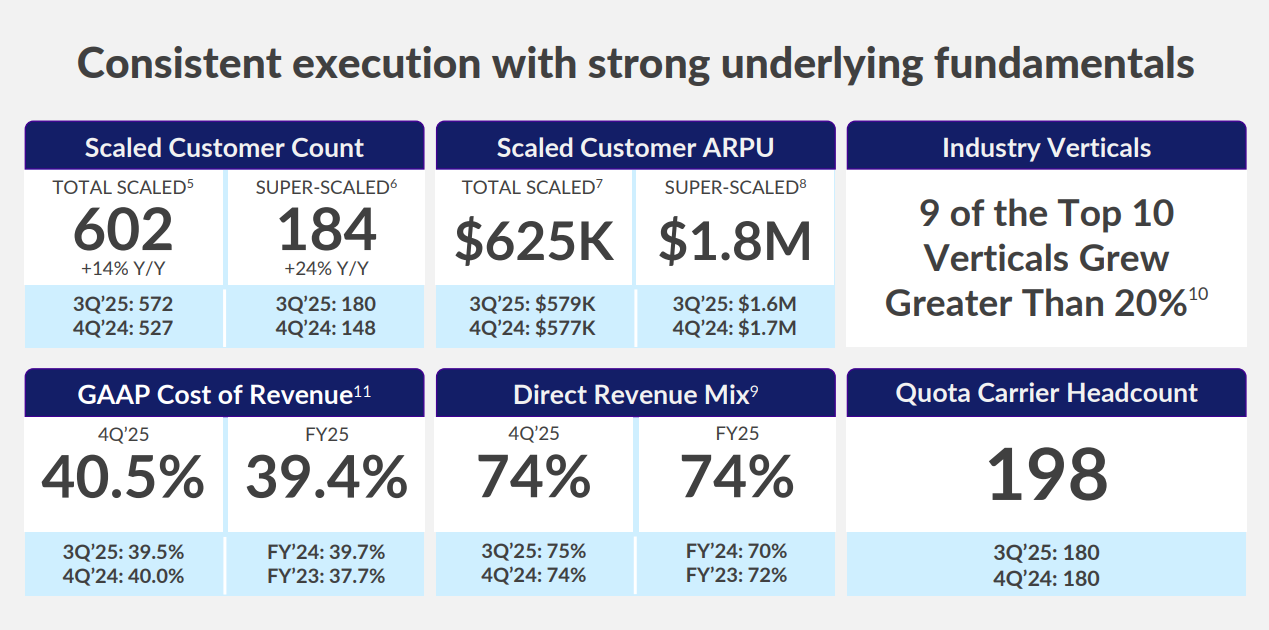

Total scaled customers grew 14% Y/Y to 602

Super scaled customers ($1M+ spend) grew 24% Y/Y to 184

Scaled customer ARPU of $625K, up 8% Y/Y

Super scaled customer ARPU of $1.8 million

9 of the top 10 industry verticals grew over 20% on a TTM basis

Direct platform revenue mix of 74%

Quota carrier headcount of 198, up from 180 Y/Y

Balance Sheet

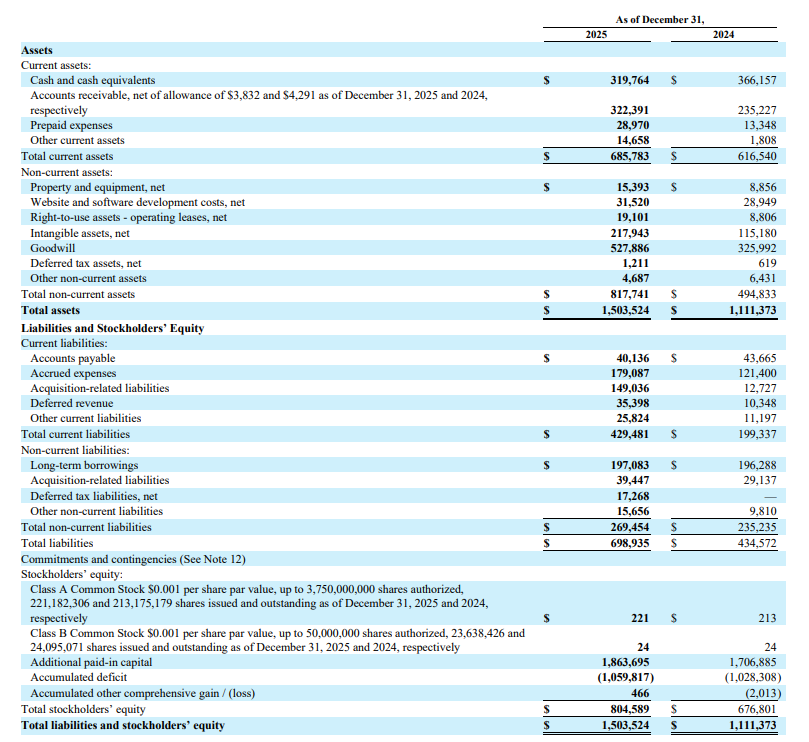

Cash and cash equivalents of $319.8 million

Long term borrowings of $197.1 million

Total assets of $1.504 billion

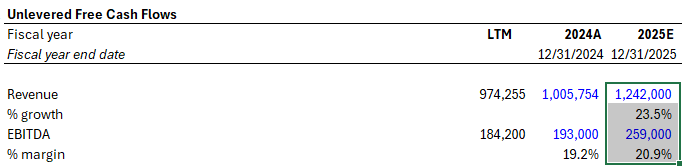

Results vs. My Prior Estimates

I’m very happy with Zeta’s FY2025. They beat both the Street and my own estimates in both revenue and EBITDA:

Revenue: $1,305M (actual) vs $1,242M (my estimate)

EBITDA: $279M (actual) vs $259M (my estimate)

This continues the pattern I highlighted in my initial report Zeta has a consistent track record of setting conservative guidance and then over-delivering. The company has now beaten revenue estimates for 18 consecutive quarters, and the magnitude of the beats has not diminished even as the revenue base has scaled past $1.3 billion. Importantly, the outperformance is not just on the top line. EBITDA margins expanded faster than expected, and the company achieved a full year FCF figure of $165M versus the $131.5M that was guided at the start of the year a remarkable 25% beat on cash flow.

Analysis of Q4 and Full Year Results

Revenue Quality Continues to Improve

What stands out most in this quarter is the quality of revenue growth. Organic revenue (excluding political, LiveIntent, and Marigold’s Enterprise Business) grew 28% in Q4 and 27% for the full year. This is not acquisition-driven headline inflation the core business is genuinely accelerating. The direct platform revenue mix held steady at 74%, which is important because direct revenue carries stronger operating leverage and is more predictable.

Vertical diversification also continued to strengthen. Nine of the top ten industry verticals grew over 20% on a TTM basis, with Travel & Hospitality, Advertising & Marketing, Automotive, Consumer & Retail, and Telecom being the five fastest growing. This breadth of contribution is a meaningful de-risking factor and reduces the company’s exposure to any single sector downturn.

Customer Economics Are Compounding

The customer metrics tell a powerful story. Super scaled customers (those generating at least $1M in TTM revenue) grew 24% Y/Y to 184. This cohort now represents approximately 90% of total revenue, up from roughly 70% at the time of the IPO. The ARPU for this group stands at $1.8M, which is approximately 17x that of the $100K–$1M scaled cohort ($104K quarterly ARPU). Super scaled customers also use an average of 3.3 channels on the platform versus 1.9 for the lower tier, confirming the thesis that deeper platform adoption drives materially higher spend.

The cohort analysis provided in the supplemental presentation further reinforces this. Customers that have been with Zeta for 5+ years generate an average ARPU of $3.9M up from $2.8M in FY2024. Meanwhile, approximately 90% of FY2025 revenue came from customers who have been with Zeta for more than one year. This stickiness, combined with an expanding wallet share, underpins the durability of the growth trajectory.

Net revenue retention hit a record 120% during FY2025, which the CEO highlighted on the earnings call. This is a significant inflection from the roughly 115% average the company has maintained historically and signals that existing customers are not only staying but accelerating their spend.

Margin Expansion Is Structural, Not Cyclical

The Adjusted EBITDA margin story deserves particular attention. Full year margins expanded 217 bps to 21.4%, and Q4 margins hit 24.1% marking the 20th consecutive quarter of Y/Y margin expansion. This is not a one-time cost-cutting exercise. The company is demonstrating genuine operating leverage as it scales. GAAP cost of revenue as a percentage of total revenue actually improved slightly to 39.4% for the full year (from 39.7% in FY2024), even as the business absorbed the LiveIntent and Marigold acquisitions.

The Q4 achievement of positive GAAP net income ($6.5M, 1.7% margin) is a notable milestone. While modest in absolute terms, this marks a turning point the company is guiding for positive GAAP net income for the full year 2026, and management indicated on the earnings call that they expect to be net income positive every quarter going forward. Stock-based compensation continued to decline as a percentage of revenue, dropping to $177.8M (13.6% of revenue) from $195.0M (19.4%) in FY2024 a meaningful improvement from the 51% ratio seen in FY2022. The trajectory here is encouraging and directly addresses one of the most common investor concerns around Zeta.

Cash Generation Is Inflecting

Free cash flow of $164.7M represented 78% growth Y/Y and a 12.6% margin, up from 9.2% in FY2024. The FCF-to-EBITDA conversion ratio of 59% is solid, and notably, the company has identified working capital headwinds from agency business growth as a temporary drag on conversion if you adjust for these, conversion rates are even higher (76% on a working-capital-adjusted basis for FY2024–FY2025). Management is guiding for $231M of FCF in 2026 and targeting $371M+ by 2028, with a 65% conversion ratio. If they achieve this, it would represent a nearly 4x increase in FCF from 2024 levels in just four years.

Earnings Call Takeaways

Athena by Zeta The AI Agent Opportunity

The CEO spent considerable time discussing Athena, Zeta’s AI agent built on top of the Zeta Marketing Platform. He described the ZMP as a “747” powerful but complex to operate and Athena as the tool that makes it easier for clients to “fly the plane.” Early adopters are reporting significant time savings on segmentation and targeting, as well as improved ROI. The company confirmed it is on track to make Athena generally available by Q1 2026.

The monetization strategy for Athena is not yet fully defined, and management was candid that they are not counting on meaningful revenue contribution from Athena in 2026 guidance. However, the CEO noted that customers are responding very positively, and the percentage of enterprise clients using more than one use case on the ZMP grew 80% Y/Y in Q4. Given that customers who adopt multiple use cases see 200–300% revenue uplift on average, Athena’s potential to accelerate cross-selling is a material upside driver that is not yet priced into guidance.

LLM Narrative

The CEO, David pushed back on the narrative that LLMs will disrupt enterprise software companies, arguing instead that they will drive efficiency gains that more than offset the cost of integration. He compared LLMs to infrastructure providers like AWS or Snowflake they become part of the technology stack rather than a competitive threat. Especially since: Zeta’s revenues are tied to volume of decisions made not seats, meaning AI driven corporate jobs cuts wont effect Zeta’s top line.

One Zeta Sales Model Gaining Traction

The “One Zeta” approach selling the platform as a unified system across data management, marketing automation, and programmatic engagement is clearly gaining momentum. The number of clients using more than one use case grew 80% Y/Y. Currently, 25% of scaled customers use more than one use case, which means there is substantial room for expansion. The CEO also highlighted a major telecom win worth $39M and noted that $40M in deals have already closed from leads generated at the Zeta Live event, with $130M of value from a pipeline of 200 opportunities.

Macro Resilience

When asked about tariff and macro risk, the CEO was direct: Zeta’s 600% ROI on ad spend doesn’t just insulate the company from economic headwinds it actively drives growth during uncertainty. Clients focused on maximizing marketing ROI are consolidating spend toward platforms that can demonstrate measurable returns, which benefits Zeta. He noted that Fortune 500 companies have shifted their focus from simple revenue-to-marketing ratios to demanding 500–1,000% ROI on ad spend, and Zeta’s platform is purpose-built to deliver on that demand.

GAAP Profitability Path

The CFO confirmed that Q4 2025 marked a turning point for GAAP profitability, with the company expecting to be GAAP net income positive every quarter from here. For FY2026, they are guiding to GAAP EPS of $0.02–$0.04. While the absolute numbers are small, this is a critical milestone for broadening the investor base and eliminating a long-standing bear argument.

What I’m Watching Going Forward

Athena Adoption Rates. While not yet in guidance, the pace of Athena rollout and its impact on cross-selling and NRR will be the most important leading indicator of whether Zeta can sustain 20%+ growth beyond 2026.

GAAP Profitability Consistency. The company has guided to positive GAAP net income for FY2026. Consistent quarterly delivery on this commitment will broaden the investor base and should support multiple expansion.

SBC Trajectory. The decline from 51% of revenue in FY2022 to 13.6% in FY2025 is encouraging, but I want to see continued progress toward the 10–12% range, which would be more in line with mature SaaS peers.

Political Revenue. The $15M guide for 2026 is deliberately conservative given the off-cycle year. Any upside here flows directly to the bottom line and could contribute to further guidance raises.

Conclusion

Zeta’s F4Q’25 results and updated guidance reinforce the investment thesis I laid out in my initial report. The company is executing on all cylinders: revenue growth is durable and broad-based, margins are expanding structurally, cash generation is inflecting sharply, and the customer economics are compounding in a way that builds the moat over time. The achievement of GAAP net income in Q4 and the commitment to full year GAAP profitability in 2026 removes a key overhang, while the Zeta 2028 targets now upgraded for the Marigold acquisition provide a clear multi-year framework that the company is tracking ahead of.

The broader SaaS sell-off has weighed on Zeta, but I believe the company is fundamentally insulated from the AI disruption fears pressuring the sector. Unlike traditional SaaS businesses that price on a per-seat basis where AI-driven workforce automation poses a direct threat to revenue Zeta’s pricing is tied to the volume of marketing decisions executed through its platform. More importantly, Zeta’s proprietary data cloud, built on 245 million US identities and trillions of signals, represents a structural moat that AI cannot easily replicate or disintermediate. If anything, AI adoption is a tailwind: as enterprises demand higher ROI on marketing spend, Zeta’s AI-powered platform becomes more valuable, not less. I expect the market to recognise this differentiation as the company continues executing into 2026, and for the multiple to re-rate accordingly. Zeta continues to prove that it can deliver durable, predictable, and profitable growth at scale, exactly what it promised.

“That’s it! Thank you very much for reading! You can subscribe and like to support my research and to receive my research right to your inbox. Please make sure to reach out if you have any questions or if you want to chat about markets.”