York Space Systems: The Most Undervalued Space Stock

York Space Systems (NYSE: YSS) is a US-based, space and defense prime

Company Snapshot

Company Overview

York Space Systems (NYSE: YSS) is a US-based, space and defense prime providing a comprehensive suite of mission-critical solutions for national security, government and commercial customers. York is one of the only space and defense primes with proprietary hardware and software capabilities designed to address complex mission requirements throughout the mission lifecycle. York is one providers to the US Department of War’s (“DoW”) Proliferated Warfighter Space Architecture (“PWSA”).

Core Business Segments

York makes money in two different ways:

Left of launch: York bids on SDA contracts as the prime, builds a satellite bus, integrates the missing specific tools into the satellite, delivers it to the launch provider, this enables the customer to operate the satellite in orbit and receive data.

Right of launch: York offers software services to operate or to allow to communicate with the satellite for its customers.

Left of launch accounts for >95% of the revenue with gross profit margins of ~35%. While the right of launch accounts for <5% of the sales but margins are ~90%.

Three types of satellites:

S-Class: York’s smallest and most flight-proven bus, designed for 85 to 200 kg and 2 kW peak power. A low-cost platform built for rapid fielding, it can be launch-ready 60 days after payload receipt and serves as the design foundation for the family.

LX-Class: Roughly double the S-Class, supporting up to 500 kg with a 1.5 kW baseline (configurable higher). It shares over 90% of its technology with the S-Class and has been York’s primary SDA platform, flight-proven 22 times, central to the PWSA Transport Layer opportunity.

M-Class: York’s largest spacecraft, introduced in 2025, supporting up to ~2,000 kg and 8 kW+ peak power. Optimized for Earth observation and communications at roughly half the cost, it shares ~75% of hardware and 95% of software with the other platforms and targets future SDA and Intelligence Community programs.

Market Positioning

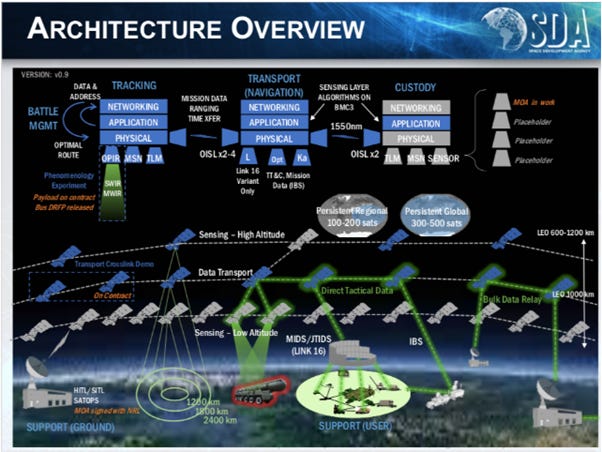

York bids on contracts from DoW PWSA and has around 35% of the market share in the transport layer.

After opening its Potomac facility, York has quadrupled production capability and believes it can manufacture and test over 1,000 satellites per year across its two facilities if Golden Dome demand surges. We have also assumed that revenue is recognized on % of completion accounting, it takes three years for a satellite to be built and launched from the date of contract being awarded.

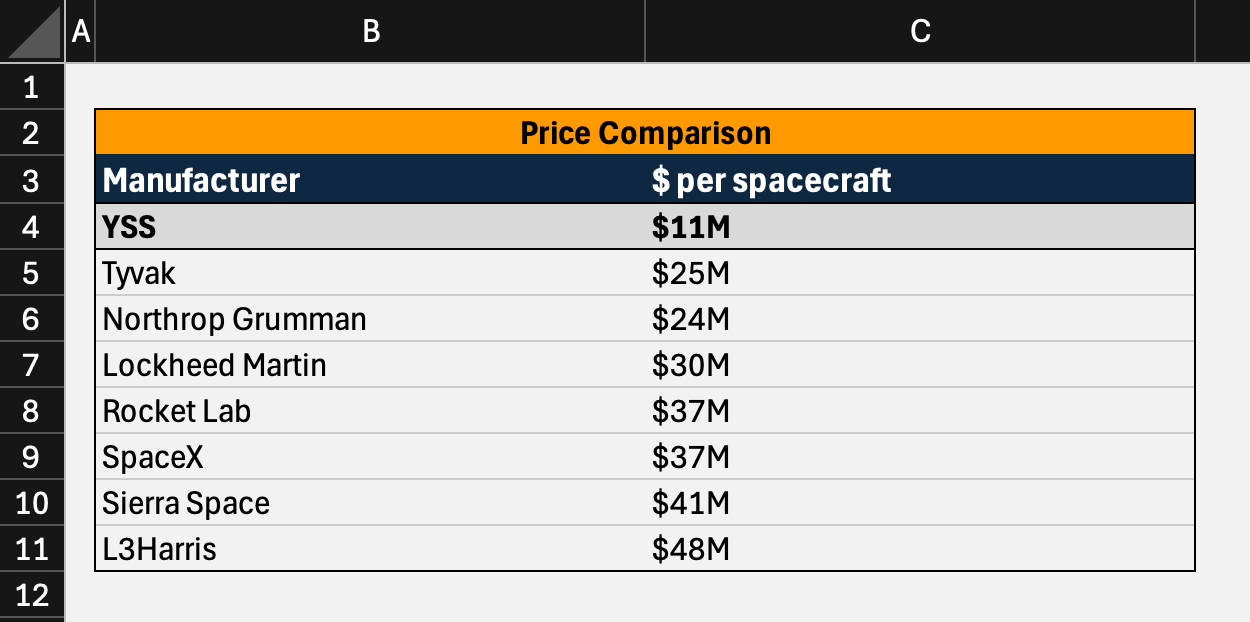

The competitive advantage of York is their cheap satellites.

York’s satellites cost roughly 50% of traditional primes’ prices, which supports its 83% win rate for satellite contracts under the SDA’s PWSA.

Business Analysis

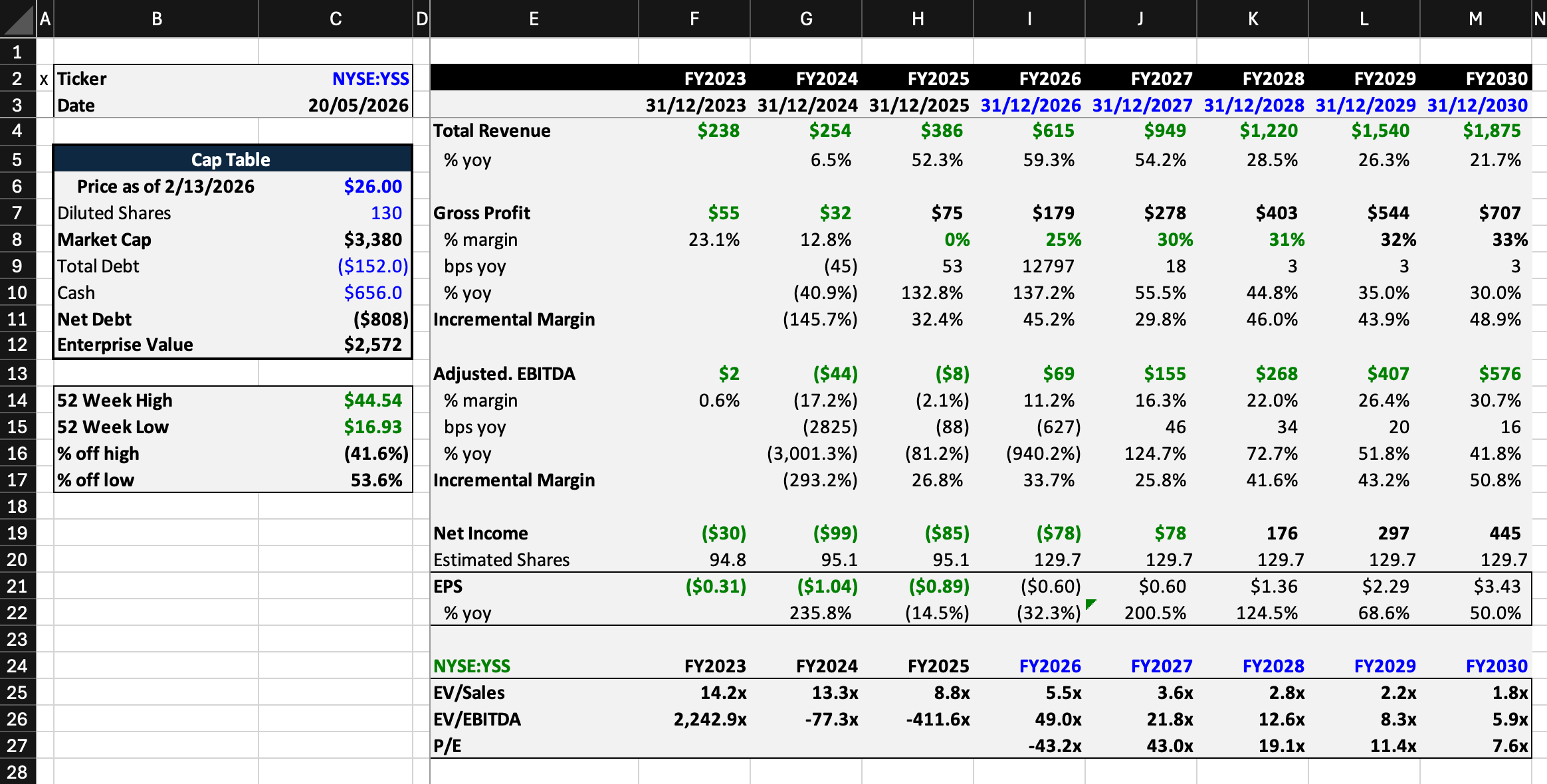

Revenue Growth

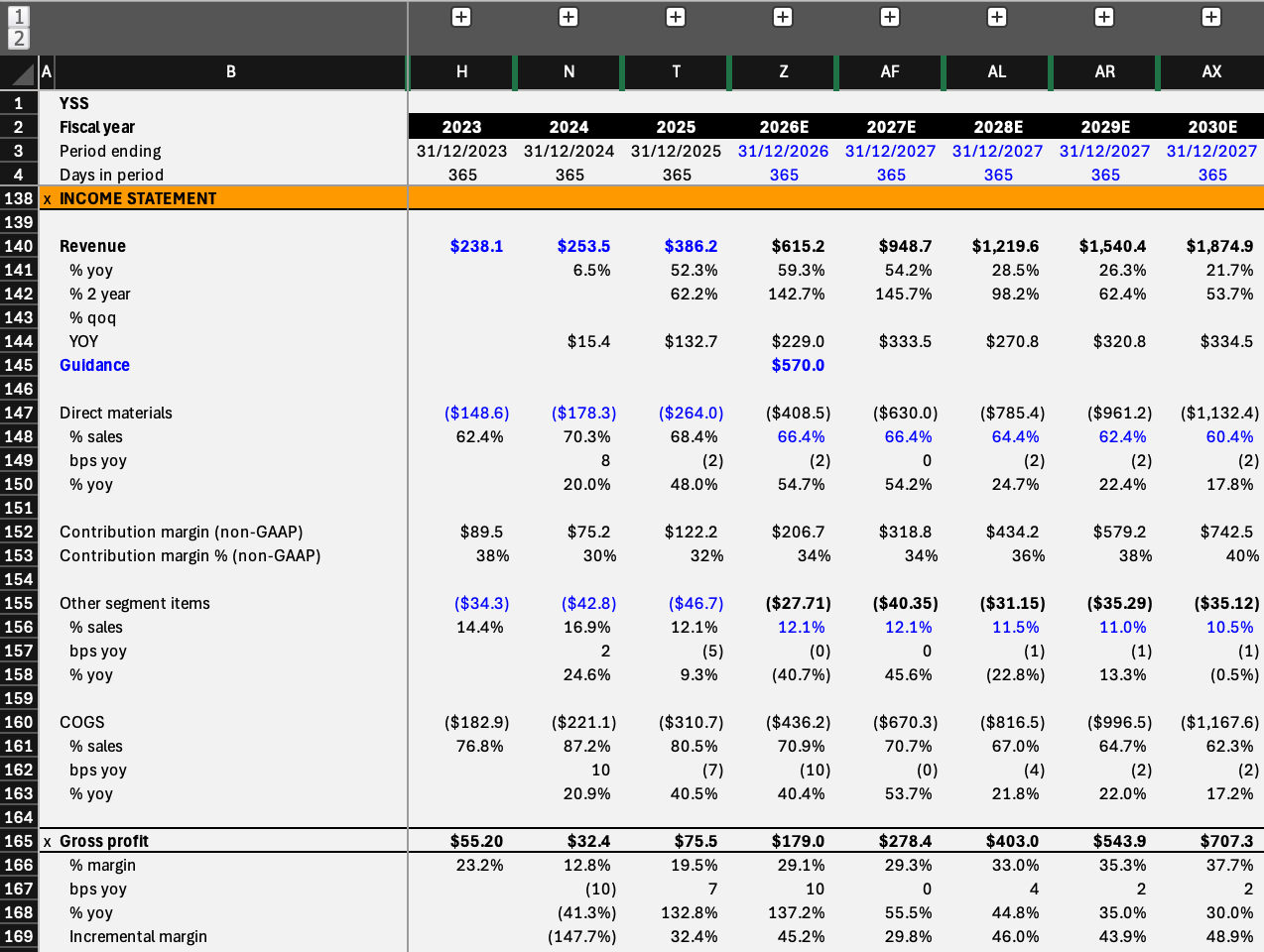

York historically is a very high growth business. Y/Y revenue growth from 2024-2025 is 51%, we’ve modelled the same growth rates going into 2026E and 2027E based on the potential from the Golden Dome project as well as growing interest from US intelligence agencies to have satellites in the orbit.

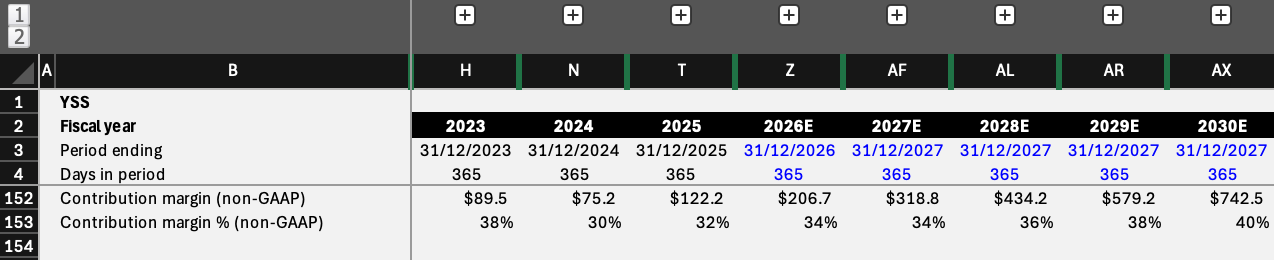

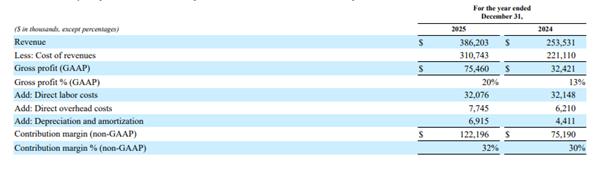

Contribution Margin

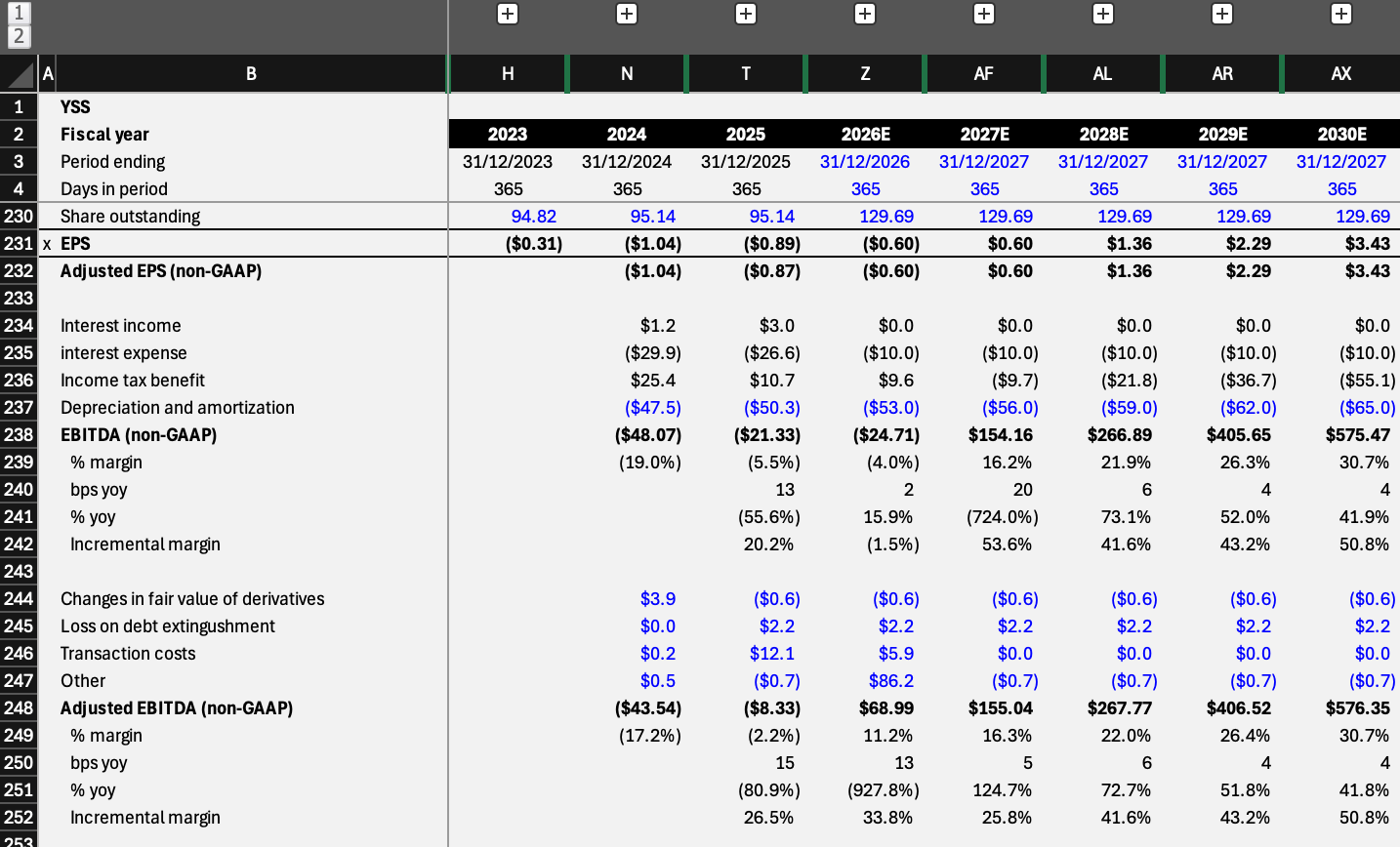

Contribution margin in 2025 on left of launch has improved to 32% from 30% in 2024. We’re projecting further improvements in contribution margin of roughly 2% per year up to 2030E.

Below is an image from York’s FY2025 10-K showing their breakdown on contribution margin:

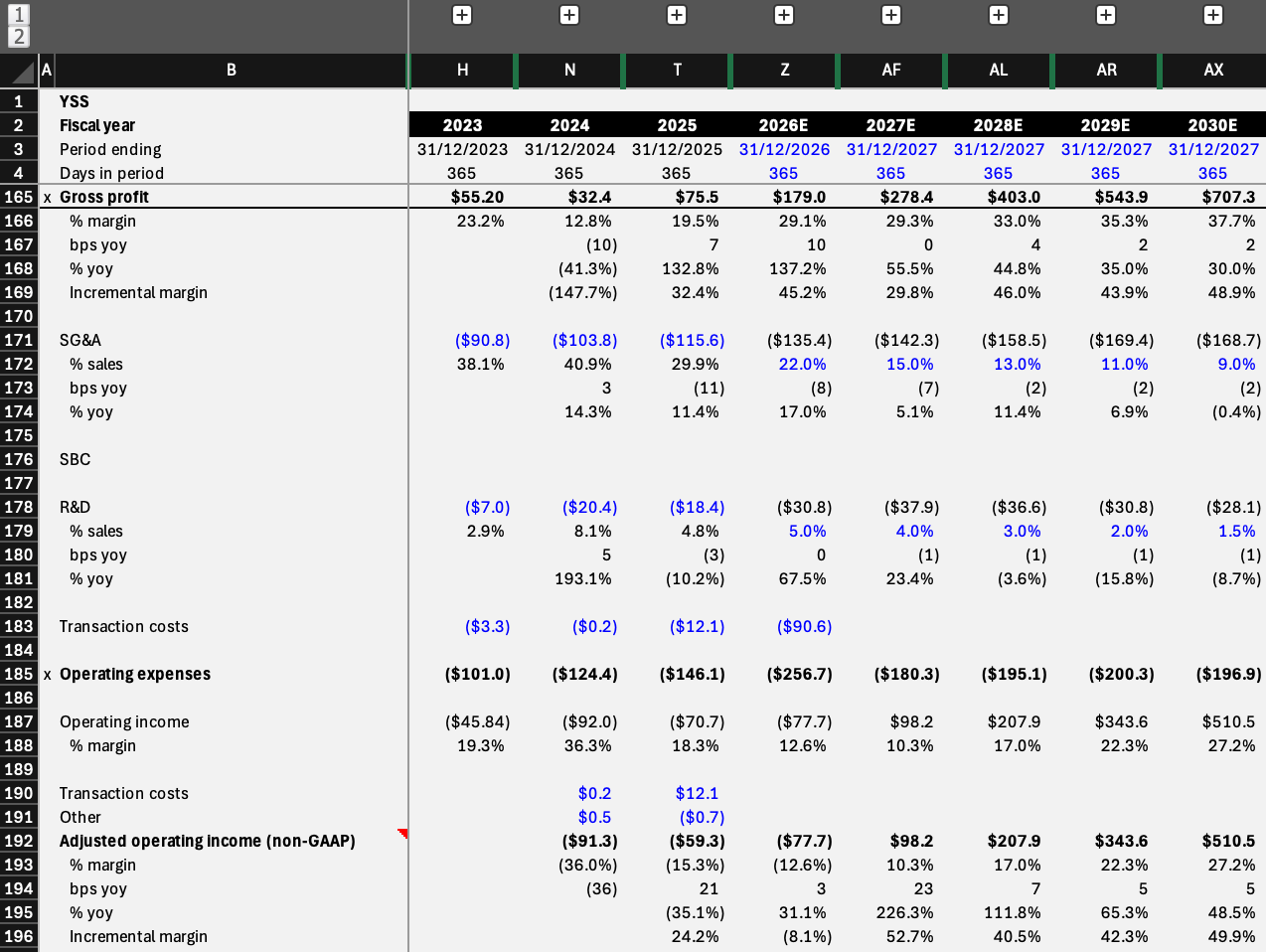

Gross Profit Margin

Gross profit margin in FY2025 sits at 19.5% up from the previous year’s 12.8%. Overall, the GPM is improving and we’re modelling a 29.5% GPM in 2026E. This increase is mainly driven by the following assumptions: 51% increase in revenue, and COGS as a % of sales falling from 80.5% in 2025 to 70.5% in 2026E.

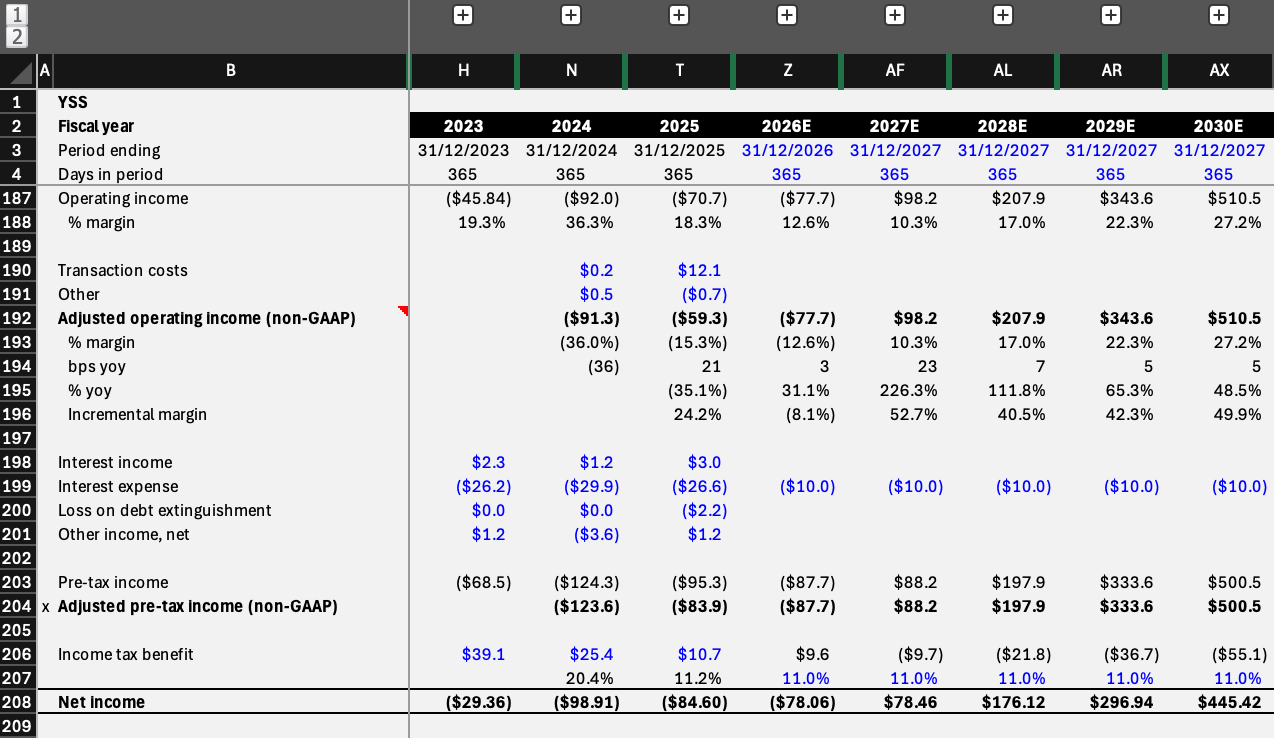

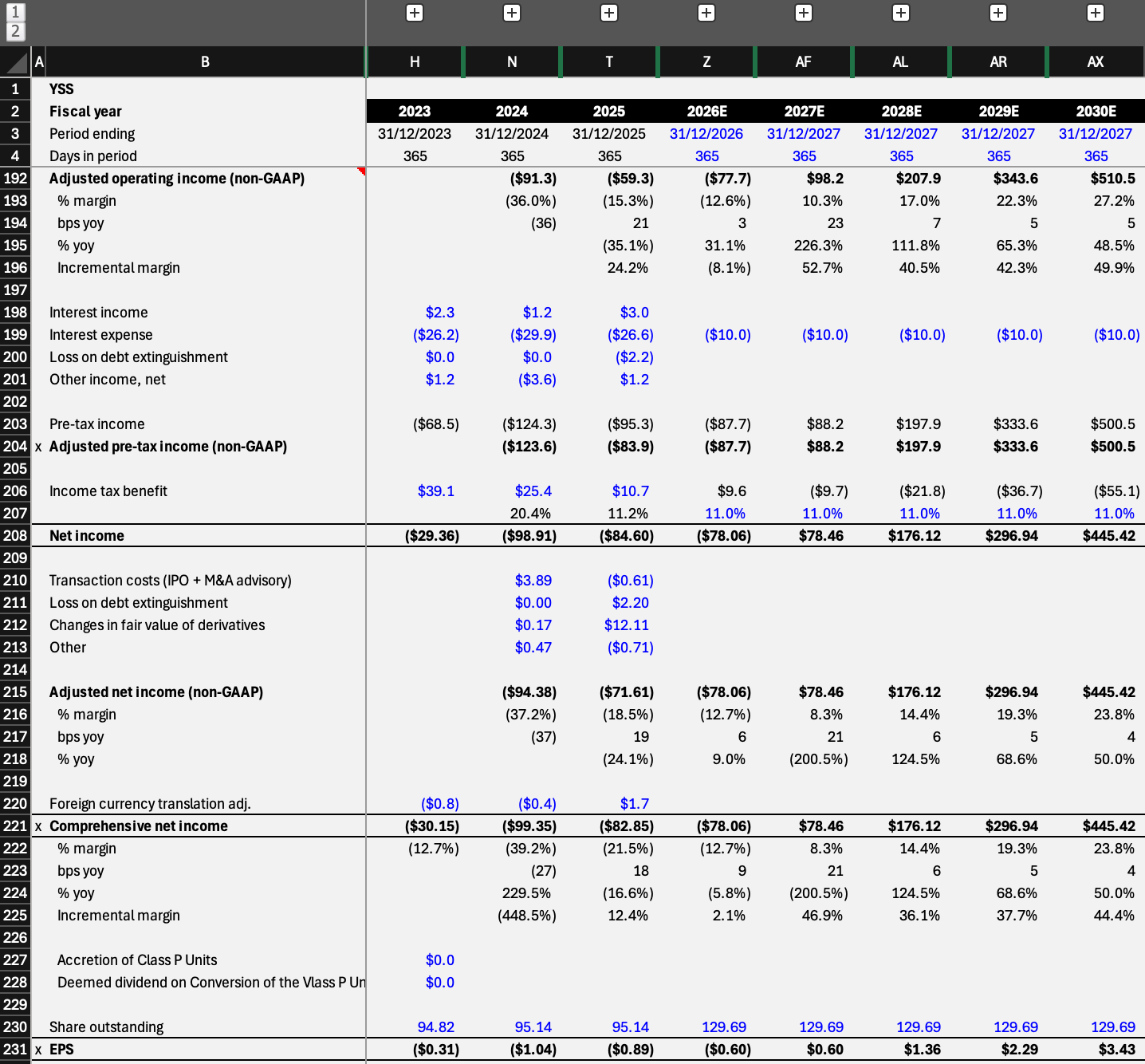

Operating Margin & Adj. Operating Margin

Operating income and adjusted operating income are expected to turn positive in FY2027. We expect a slight degradation of operating margin to low teens based on the costs associated with the recent IPO. Adjusted operating income is modelled to improve every year until 2030E.

Capital Intensity

York is a capital light business that invests around 5% of its revenue in R&D because they have the three-class satellite infrastructure built out. We model this number to fall as the total revenue grows and the need to further invest in R&D stays stagnant due to great market fit of York’s products.

Capital Deployment

York went public in January 2026, and within weeks began an aggressive M&A campaign funded largely by its ~$583m of IPO net proceeds. On March 6, 2026 about five weeks after the IPO it acquired Orbion Space Technology, it is a Michigan-based maker of flight-proven electric propulsion systems, for ~$74.9m (roughly $11.2m cash and ~$60.2m in stock at $34/share). It followed that on April 29, 2026 with a definitive agreement to acquire All.Space for $355m (~$155m cash and up to 5.9m shares), expected to close in 2H26. York had also earlier brought in ATLAS Space Operations, a ground-software-as-a-service provider, via common-control transactions in August 2025 ahead of the IPO. So York has remained aggressive in M&A and leveraged its dry powder to acquire companies rather than spending capital and years building certain systems and infrastructure.

Financial Model Summary and Key Drivers

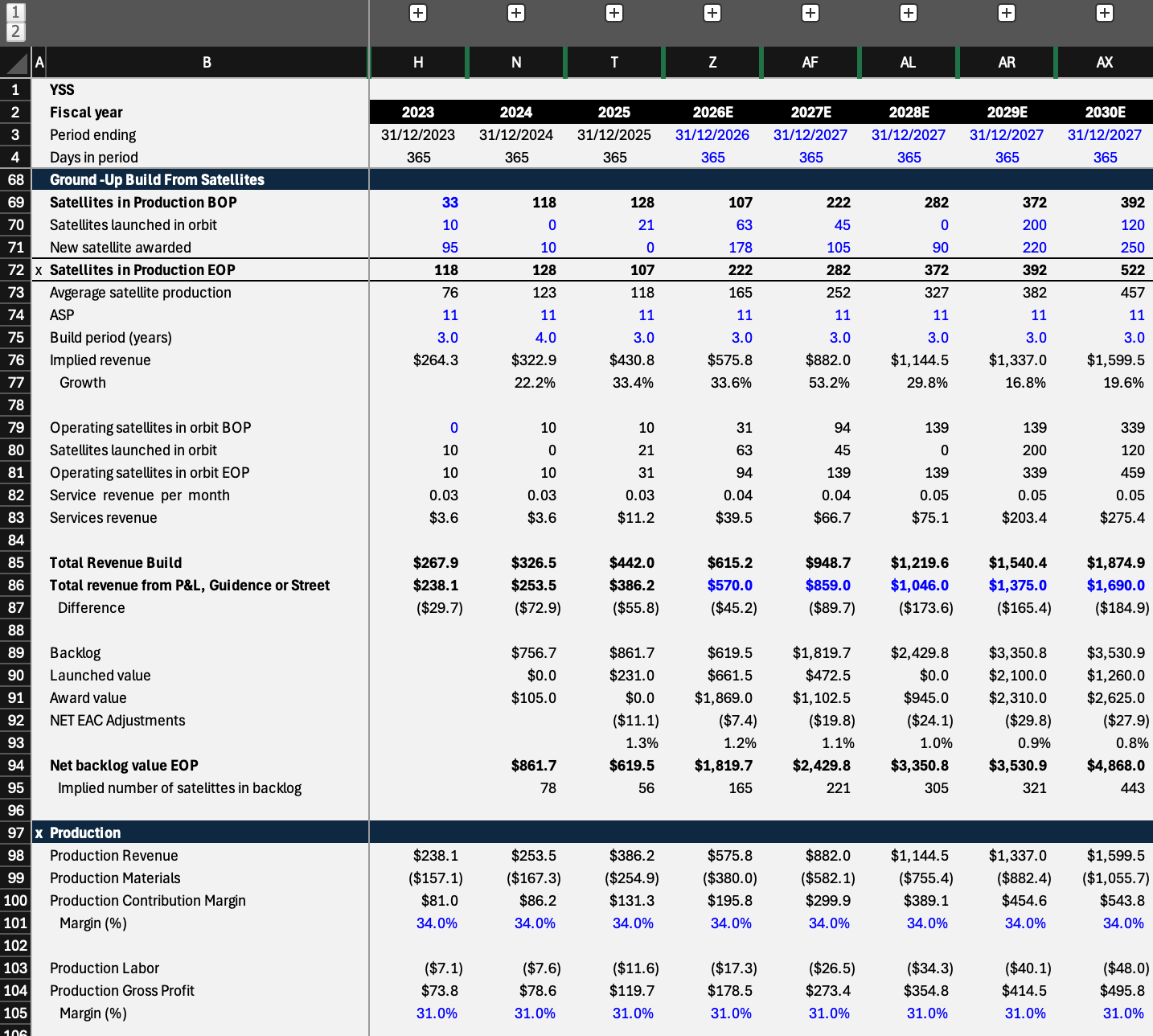

Revenue Build

P&L

EPS & EBITDA

3 Key Drivers

1. New satellite awards

2. Gross margin

3. Operating margin

New Satellite Awards

Satellite awards create backlog which creates (relatively) stable revenue. In Q1’26 York was unable to get any new satellite awards. The reason wasn’t that York bid and lost, (YSS wins 83% of contracts they bid on) it’s mostly that the awards York is targeting simply hadn’t come up for award yet in Q1. The explanation, pieced together from management’s commentary, is about timing of the procurement cycle, not a competitive failure.

The big PWSA opportunity York is chasing, the Tranche 3 Transport Layer (T3TL) is anticipated to be announced in 2026, thus it wasn’t awardable in Q1. The most recent SDA award that did happen, the Tranche 3 Tracking Layer in December 2025, was a layer York didn’t participate in (it focuses on the Transport Layer). So, there was no major PWSA Transport award on the table to win in the quarter.

Gross margin & Operating Margin

In Q1’ 26 York beat street revenue estimates at $116m, but the stock price fell ~20%. The problem was margins and the bottom line. GAAP gross margin fell to 19% from 23% a year earlier, and adjusted EBITDA came in at negative $3.6m. The company cited cost overruns on one of its government contracts on materials and labor. Since contracts are fixed-price contracts, controlling the costs is essential for maintaining profitability. York had to renegotiate the contract that raised material and labor costs in exchange for being able to deliver.

Variant Perspectives

We differ from the Street in two places, both of which we think the market got wrong after the Q1’26 selloff.

On margins, consensus is treating the Q1 gross margin drop and negative EBITDA as the start of structural pressure in a fixed-price model. We don’t see it that way. The overrun hit one contract, and York has already renegotiated it, so the drag doesn’t carry forward. And Q1 was a low-volume quarter. As production scales across the backlog, fixed costs spread over more revenue and execution improves with repetition, both of which favor York’s standardized-bus model. We model gross and operating margins expanding above the Street from here. If we’re right, the market is anchoring to a trough quarter and missing the operating leverage in the business.

On new awards, the Street read the zero-bookings quarter as a red flag. We read it as the procurement calendar, not a competitive problem. York wins about 83% of what it bids and didn’t lose anything in Q1; the Transport Layer awards it targets simply hadn’t come up yet, and the one SDA award that did land was in a layer York doesn’t play in. We expect bookings to reaccelerate as the PWSA Tranche 3 Transport Layer comes up for award later in 2026.

Golden Dome is the piece we think consensus is underweighting. As the architecture gets defined and funded, it should pull forward and broaden the Transport Layer and missile-defense work York can win, on top of the existing PWSA pipeline. Put the normalizing award calendar and Golden Dome together and York returns to backlog growth faster than the Street assumes, which is what drives our above-consensus revenue and margin numbers.

Valuation

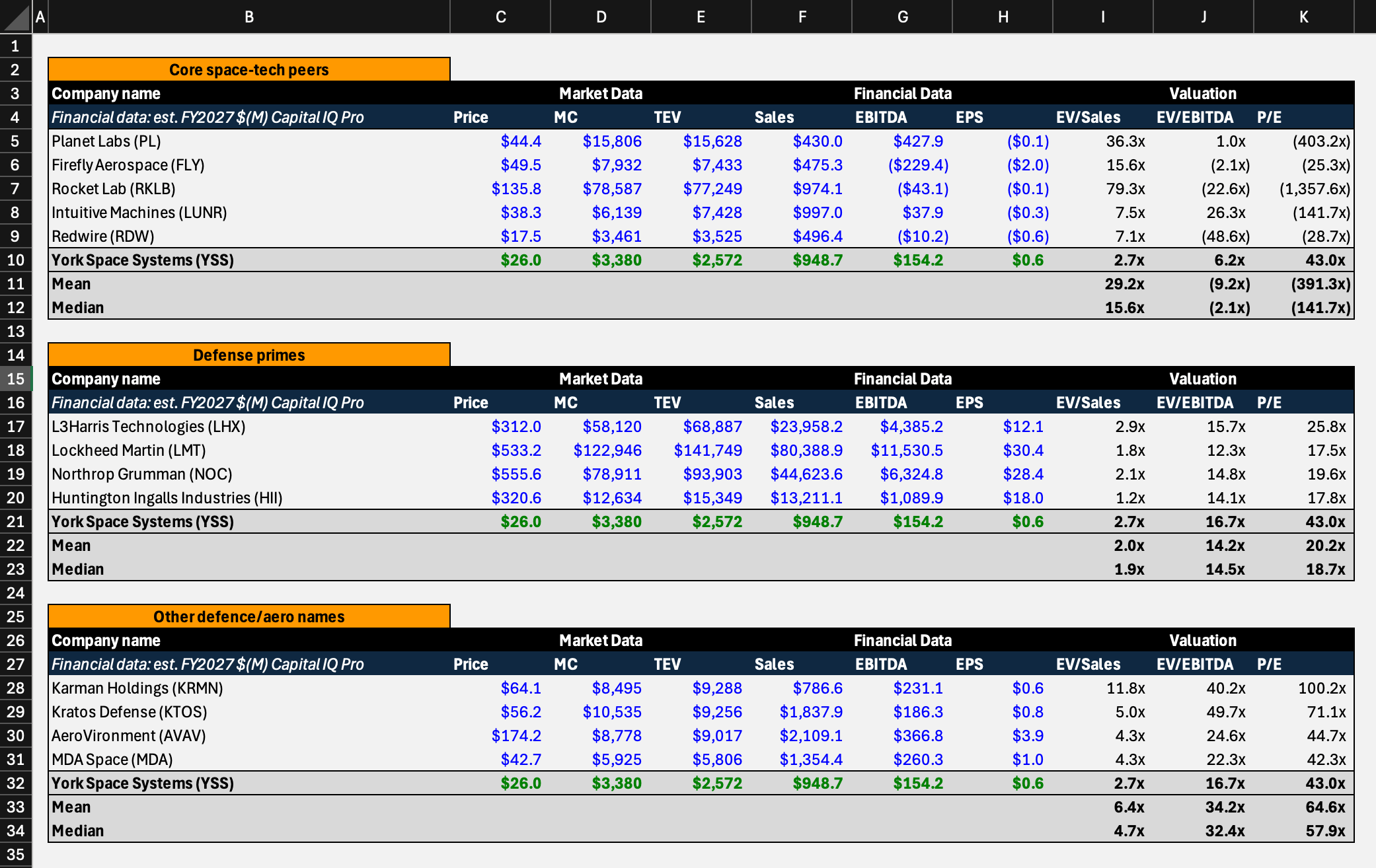

Core space-tech peers

Valuation looks attractive at these levels. York trades at a far lower EV/Sales ratio than its peers in the space-tech industry. EV/Sales ratio for York on FY2027 earnings in 2.7x while the sector mean is 29.2x and median is 15.6x.

Defense primes

Even measured against the mature defense primes, companies growing far slower than York the stock screens cheap. York’s 2.7x EV/Sales on FY2027 estimates compares to a prime mean of 2.0x and median of 1.9x, a modest premium that looks more than justified given York’s substantially higher growth profile. On EV/EBITDA, however, York’s 16.7x sits above the primes’ 14.2x mean, reflecting its earlier-stage margins; as profitability scales, that gap should compress in York’s favor.

Other defense/aero names

Against the broader defense and aerospace set, York again looks inexpensive on a revenue basis. Its 2.7x EV/Sales on FY2027 estimate is well below the group mean of 6.4x and median of 4.7x. On EV/EBITDA the picture is more balanced, York’s 16.7x is below the group’s 34.2x mean and 32.4x median, suggesting York is not being overvalued on a cash-earnings basis relative to these comparables either.

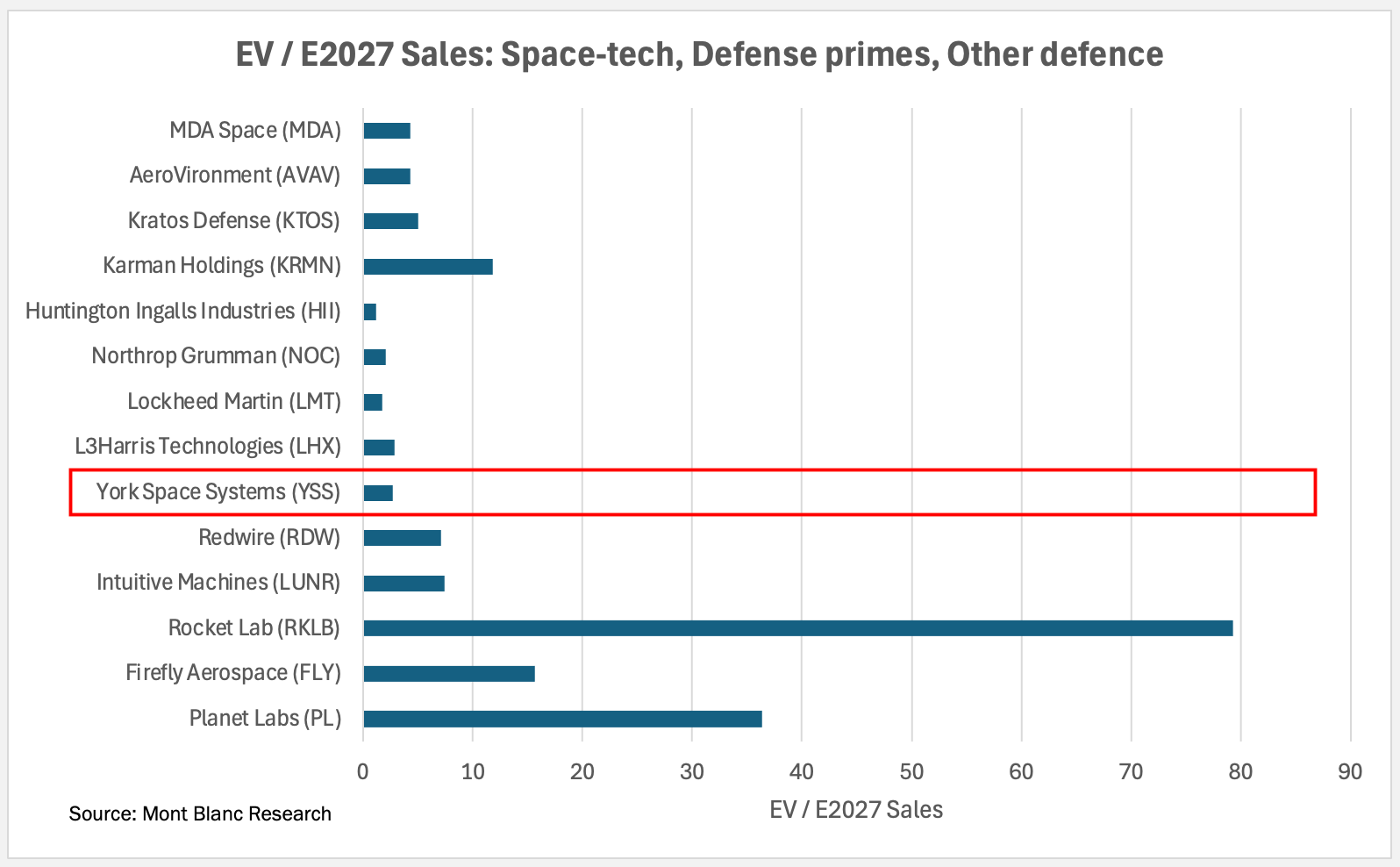

EV / E2027 Sales: Space-tech, Defense primes, Other defense

York screens as one of the cheapest names in the entire comparison set on a forward revenue basis. At 2.7x EV/2027E sales, York trades below every space-tech peer in the chart, a fraction of Rocket Lab (RKLB) at ~79x, Planet Labs (PL) at ~36x, Firefly (FLY) at ~16x, and even the closest space-tech names Intuitive Machines (LUNR) and Redwire (RDW) at ~7x. York also trades roughly in line with or below the mature defense primes (L3Harris, Lockheed, Northrop, Huntington Ingalls), all of which sit in the 1 to 3x range despite growing at a small fraction of York’s rate. For a company with York’s top-line trajectory to be valued like a slow-growth prime, and well beneath every high-growth space peer, points to a clear valuation disconnect.

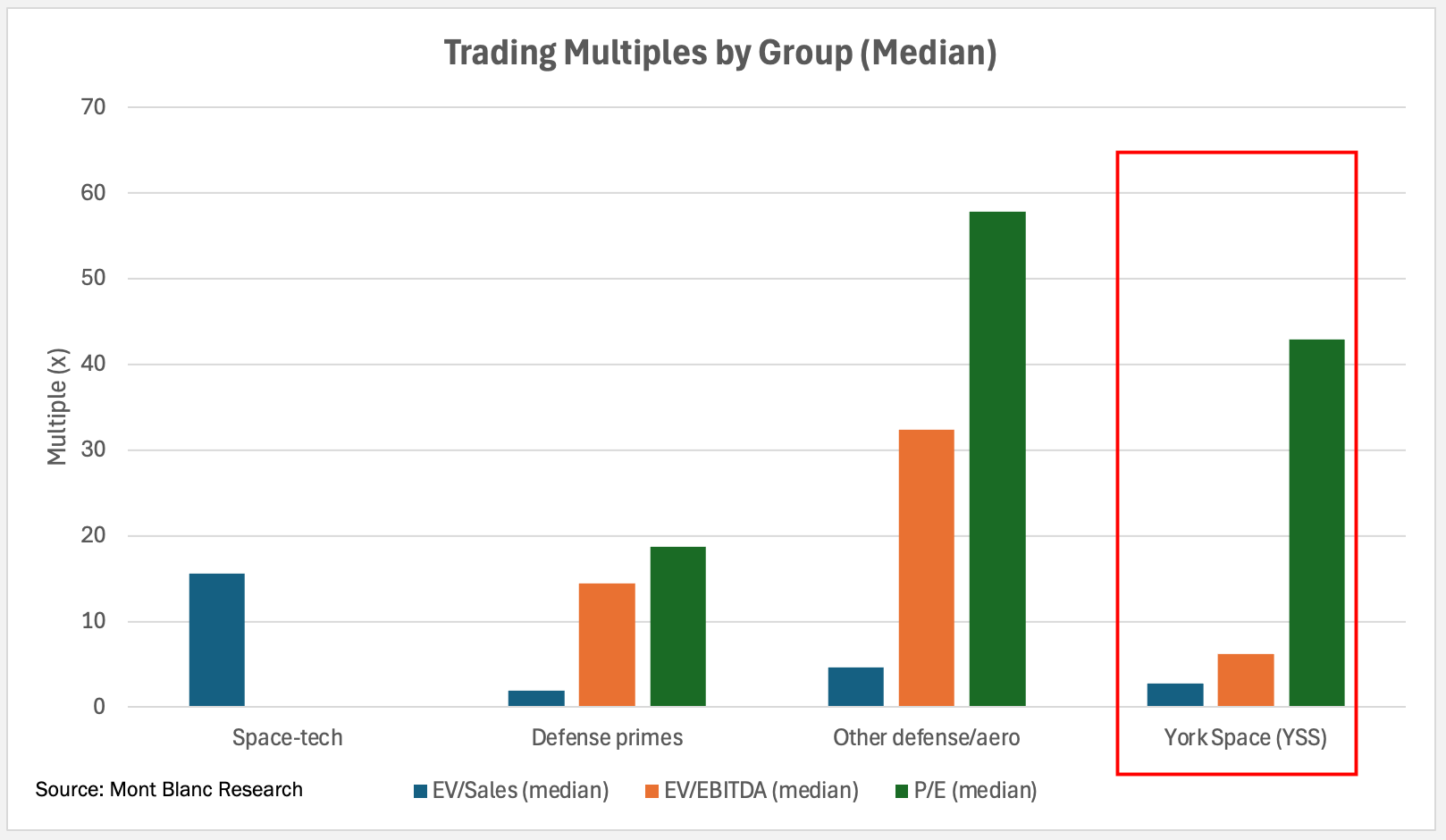

Trading Multiples by Group (Median)

This view reinforces the same story across all three multiples. On EV/Sales, York’s 2.7x median sits just above the defense primes (1.9x) and well below the space-tech and other defense/aero groups, despite York’s superior growth profile. On EV/EBITDA, York at 6.2x is dramatically cheaper than both the defense primes (~14.5x) and the other defense/aero group (~32x). That is notable because York in 2027 is projected to be positive EBITDA while much of the space-tech cohort is not, which is why that group has no meaningful EV/EBITDA or P/E bar to show. On P/E, York’s ~43x is below the other defense/aero median (~58x) and reflects its early-stage earnings base. Taken together, the chart shows York being valued like a low-growth defense prime on revenue, while screening cheap-to-mid on cash earnings, an inconsistent setup for a company with York’s growth that argues for multiple re-rating as profitability scales.

PT

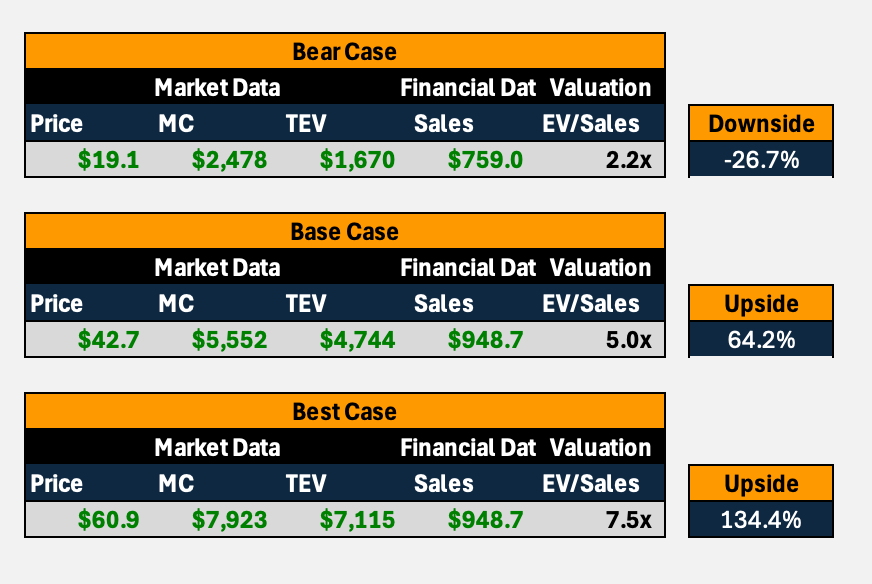

We set our 12-month price target at $43, implying roughly 67% upside from current levels. The target sits just above our base case and reflects our conviction that York re-rates as the procurement calendar normalizes and margins rise above the Street.

Our base case of $42.7 applies a 5.0x EV/Sales multiple to our 2027 sales estimate of $948.7m, generating 64.2% upside. We view 5.0x as the right anchor, it carries a clear premium to the defense primes, justified by York’s faster growth, at the same time sitting well below where the high-growth space-tech trades.

The bear case of $19.1 (down 26.7%) assumes a 2.2x EV/Sales multiple on a lower $759.0m sales figure. This is effectively York being valued like a slow-growth defense prime, the outcome if new awards stay slow, Tranche 3 Transport slips, and the Q1 margin pressure proves more persistent than we expect.

The best case of $60.9 (up 134.4%) applies a 7.5x EV/Sales multiple to the same $948.7m base. This is the scenario where Golden Dome accelerates the award cycle, York compounds backlog faster than expected, and the market begins to value it on space-tech rather than prime multiples.

The asymmetry is the key here, the upside to our best case is roughly four times the downside to our bear case, which is the kind of risk/reward skew that supports our PT of $43.

Catalysts

We see several near-term events that could drive the stock as our thesis plays out.

Jefferies Space Virtual Summit (May 26, 2026). CEO Dirk Wallinger presents today at 2pm ET, and York has flagged that it may disclose material developments affecting the business during the event. With the stock still recovering from the Q1 reaction, any commentary on the award pipeline or margin trajectory could move shares.

Q2 2026 earnings. This is the most important near-term catalyst for our variant view. We are looking for confirmation that Q1 margin pressure was contract-specific and transitory, with gross and operating margin recovering, alongside evidence that the booking cadence has resumed. New contract awards in the quarter would directly validate our argument that the Q1 gap was timing rather than competitive weakness.

New contract awards and IDIQ wins. York has already announced multiple IDIQ awards across two national security mission areas, and we expect the booking momentum to build as the PWSA Tranche 3 Transport Layer approaches award later in 2026. Each award adds to backlog and reinforces the revenue visibility that underpins our above-Street estimates.

Golden Dome developments. Further definition and funding of the Golden Dome architecture is the upside accelerant we think consensus is underweighting. Concrete progress, including specific awards beginning to flow from the DoW, would pull forward and broaden the Transport Layer and missile-defense work York is positioned to win.

Expanded DoW satellite budget. Incremental funding for proliferated LEO satellites in the defense budget would lift the total opportunity set across the SDA pipeline and improve the odds of York hitting the higher end of our award assumptions.

SpaceX IPO. A high-profile SpaceX listing would refocus investor attention and capital on the space sector broadly, and a richly valued debut could pull peer multiples higher, supporting the re-rating toward space-tech multiples embedded in our best case.

All.Space acquisition close. York’s pending acquisition of satellite communications terminal provider All.Space is expected to close in Q3. Completion would broaden York’s multi-orbit communications capabilities and add a new growth vector beyond the core satellite-bus business, with deal close itself a discrete catalyst.

Conclusion

York is a misunderstood opportunity. It trades at 2.7x EV/2027E sales, cheaper than every high-growth space peer and roughly in line with slow-growth defense primes, despite a growth profile that resembles neither. The market has priced York like a prime when it is in fact a share-gaining, vertically integrated manufacturer.

The gap exists because the market over-read a single weak quarter. The Q1 margin pressure was a contract overrun York has already renegotiated, not structural damage to the fixed-price model, and the lack of new bookings reflected the procurement calendar rather than any competitive loss. As the award cycle normalizes around PWSA Tranche 3 Transport, margins inflect above the Street, and Golden Dome accelerates the 2026 to 2027 award flow, we expect both numbers and multiple to re-rate. The risk/reward reflects this, with roughly 134% upside to our best case against about 27% downside to our bear case.

We rate York a Buy with a 12-month price target of $43, implying roughly 67% upside, based on a 5.0x EV/Sales multiple on our 2027 sales estimate of $948.7m. We would treat this as a volatile position and size it accordingly, since customer and program concentration remains the key risk. Current levels near $26 are an attractive entry. We would revisit the thesis if York fails to win meaningful Tranche 3 Transport share, margin pressure proves structural, or Golden Dome funding slips materially.

I’ve been looking for research for York for a while, thank you!

Love this. Thanks for highlighting. It’s going on my watchlist!