Red Cat Holdings (Q4'25 Earnings Review)

Year of Record Q4 Revenue and Massive Manufacturing Scale-Up

From my initial report about RCAT in December the stock is up ~(+115%).

I’m very happy with Red Cat’s full year earnings print. (RCAT) Delivered Record Q4 Revenue of $26.2M, Full-Year Revenue Up 161% Y/Y; Massive Manufacturing Scale-Up which Positions Company for Breakout 2026.

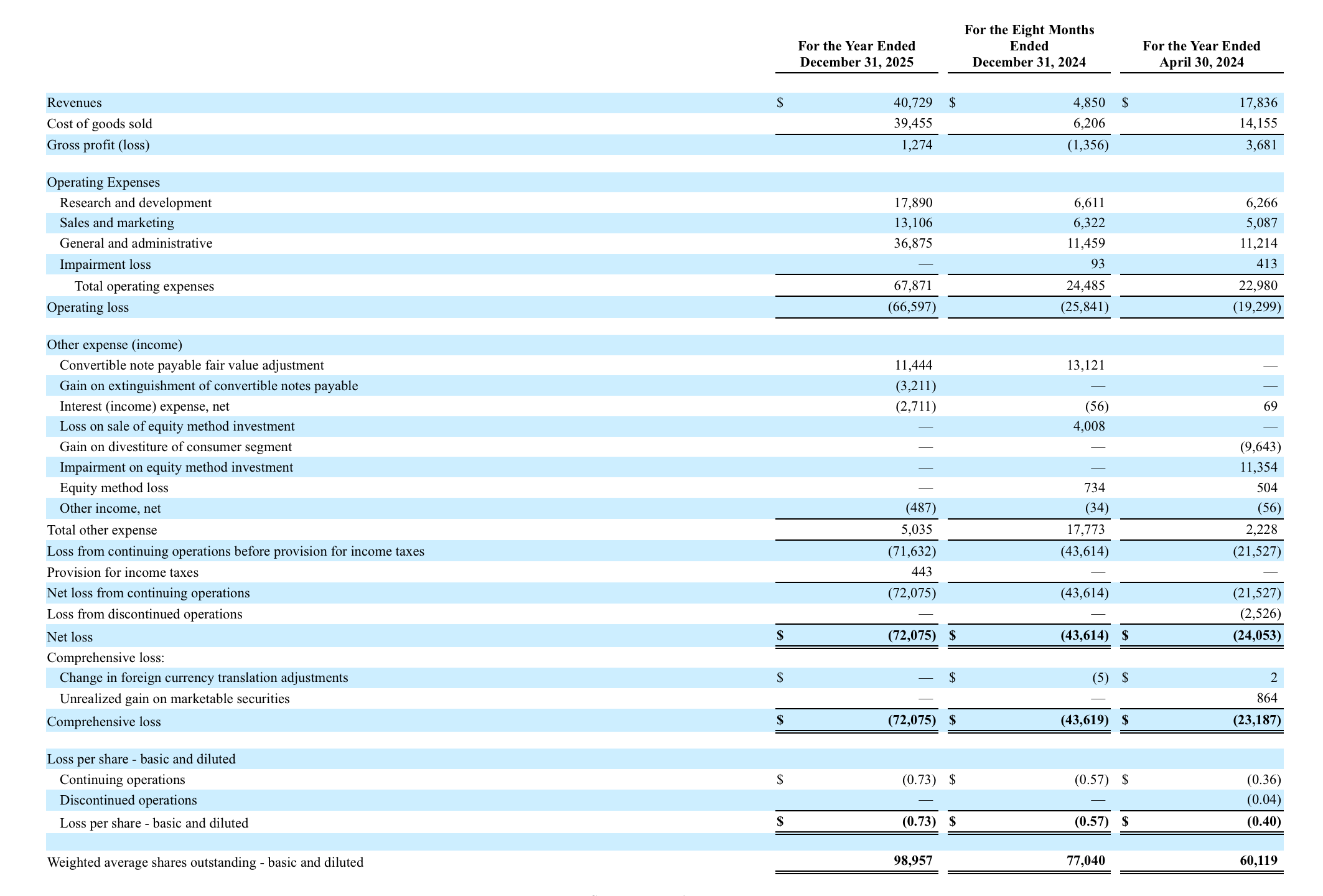

Financial Results For FY2025

Revenue

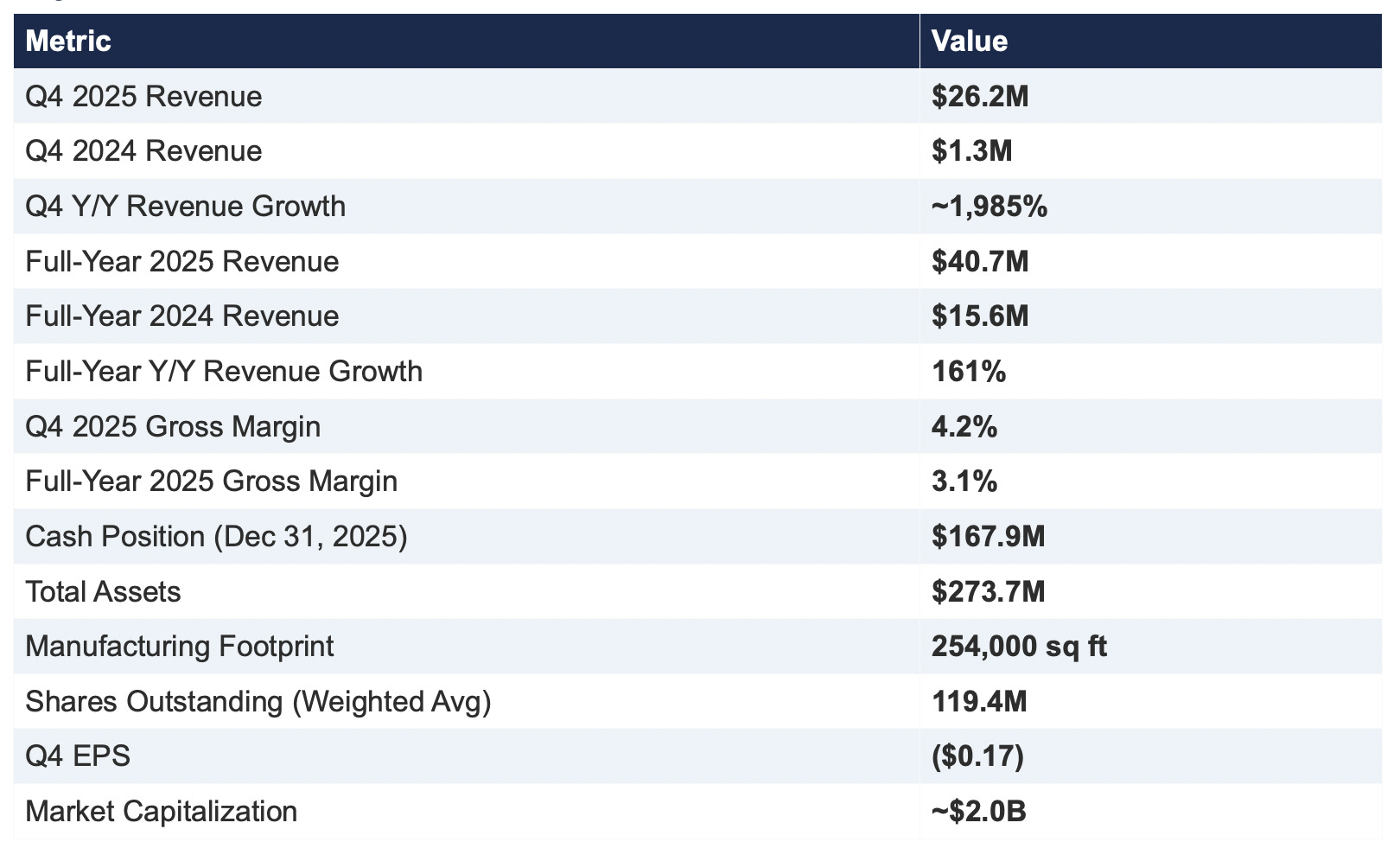

Fourth quarter 2025 total revenue of $26.2 million, up ~1,985% Y/Y from $1.3 million in Q4 2024

Q4 revenue increased sequentially by 172% from $9.6 million in Q3 2025

Full-year 2025 total revenue of $40.7 million, up 161% Y/Y from $15.6 million in FY2024

Q4 annualized revenue run rate exceeded $100 million

Revenue beat: Q4 actual of $26.2M vs. consensus estimate of $20.9M, a 25%+ revenue surprise

Profitability

Q4 gross profit of $1.1 million vs. gross loss of ($1.0M) in Q4 2024 a meaningful inflection to positive territory

Q4 gross margin of 4.2%, up ~85% Y/Y, though down sequentially reflecting mix and ramp dynamics

Full-year gross margin of 3.1%, up 332 bps Y/Y, driven by scale benefits and manufacturing improvements

Q4 Adjusted EBITDA of ($17.8M) vs. ($9.2M) in Q4 2024, reflecting deliberate investment in headcount and capacity

Full-year net loss of ($72.1M) vs. ($53.5M), driven by planned expansion spending across all domains

Q4 EPS of ($0.17), an improvement from ($0.33) in Q4 2024 despite the wider loss base

Operating Expenses & Investment

Full-year operating expenses of $67.9 million, up from $32.9 million in FY2024

R&D spend of $17.9 million, up 122% Y/Y investments in AI/ML, autonomy, and cross-domain interoperability

Headcount increased 85% Y/Y, focused on engineers and corporate functions to support growth

Stock-based compensation of $10.6 million (26% of revenue) vs. $5.7 million (37% of revenue) in FY2024

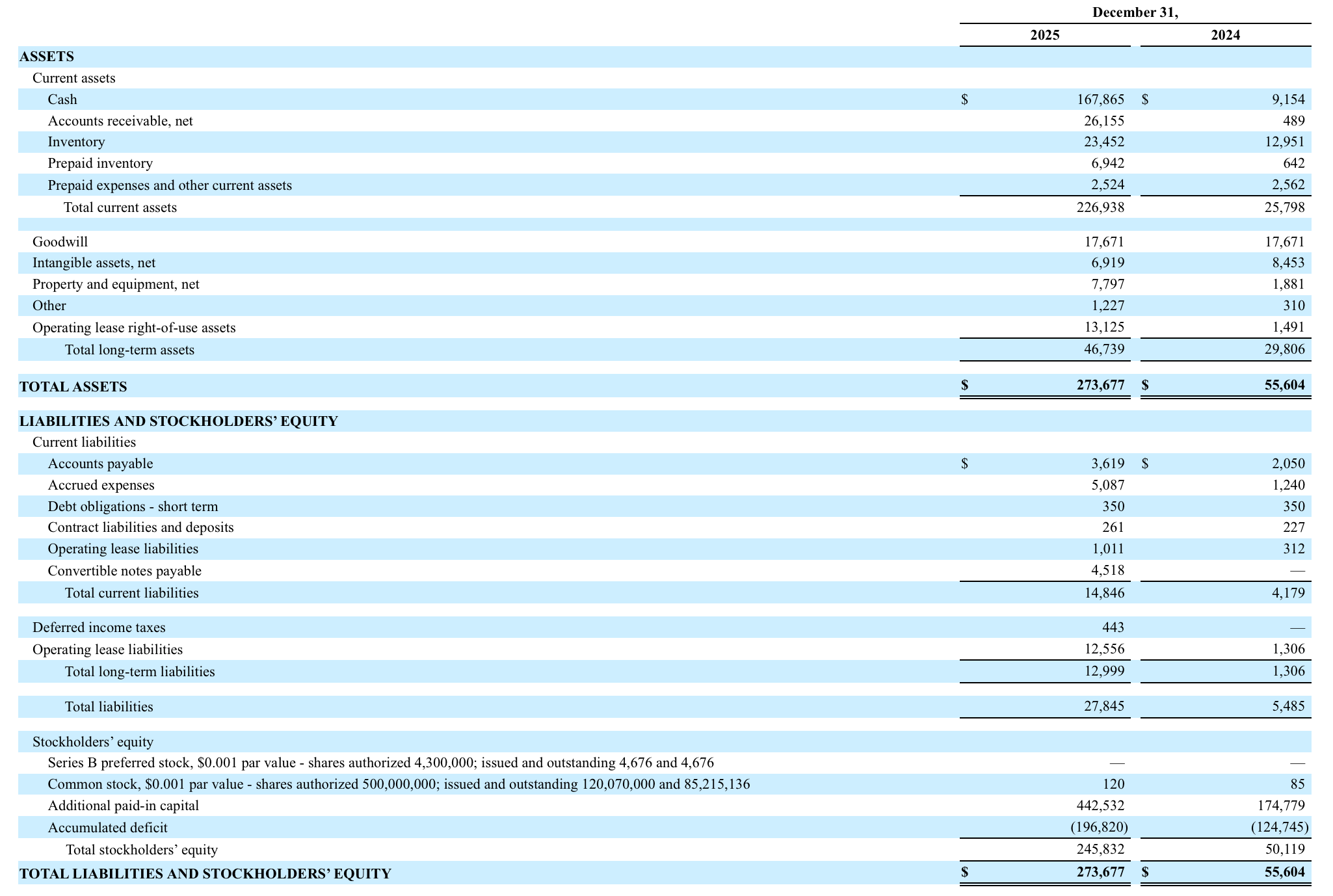

Balance Sheet

Cash and cash equivalents of $167.9 million, up from $9.2 million at year-end 2024

Accounts receivable of $26.2 million, up from $0.5 million reflecting rapid revenue scaling

Inventory and prepaid inventory of $30.4 million, up from $13.6 million proactive supply chain positioning

Total assets of $273.7 million, up from $55.6 million

Convertible notes payable of $4.5 million; long-term operating lease liabilities of $12.6 million

Stockholders’ equity of $245.8 million, up from $50.1 million

Accumulated deficit of ($196.8M)

Key Financial Metrics at a Glance:

Analysis of Q4 and Full Year Results

Revenue Trajectory: From Startup to Scale

The headline number is extraordinary: Q4 revenue of $26.2 million represents roughly a 20x increase over Q4 2024’s $1.3 million. While this percentage growth is eye-catching primarily because of the low prior-year base, the sequential story is arguably more instructive. Revenue grew 172% from Q3 to Q4, accelerating from the $9.6 million reported last quarter. This is not a seasonal blip; it reflects a genuine production ramp as Red Cat’s expanded manufacturing facilities came online and key defense programs moved from development into delivery.

The full-year number of $40.7 million, up 161% Y/Y, tells the story of a company that was largely pre-revenue at scale 12 months ago and is now delivering real product at real volume. The Q4 annualized run rate exceeds $100 million, which is significant because it provides a credible foundation for the Street’s 2026 revenue estimates in the $100-170 million range.

Perhaps most importantly, the revenue beat was substantial. Consensus expected approximately $20.9 million for Q4, and Red Cat delivered $26.2 million a 25%+ revenue surprise. For a company at this stage, beating by that magnitude signals that demand is not the bottleneck; production capacity and contract timing are.

Gross Margins: Positive but Early

Red Cat achieved positive gross margins for both Q4 (4.2%) and the full year (3.1%), which represents a meaningful inflection from the negative gross margin territory the company occupied in FY2024. The year-over-year improvement of 332 basis points at the full-year level is encouraging.

However, margins remain thin, and the sequential decline from Q3 reflects the reality of ramping new production lines, absorbing fixed costs in facilities that are not yet at full utilization, and the mix dynamics inherent in early-stage defense manufacturing. Management acknowledged that gross margins will remain volatile on a quarter-to-quarter basis as they scale. The critical question for 2026 is whether the company can begin demonstrating operating leverage as production volumes increase particularly as the Black Widow line scales toward 1,000 units per month and USV production begins.

Cash Position: War Chest Assembled

The transformation of the balance sheet over the past year is remarkable. Cash grew from $9.2 million to $167.9 million, primarily driven by a $234 million equity raise and $7.4 million from option/warrant exercises, partially offset by $89 million in operating cash burn and $6.6 million in capex. While the company is clearly burning cash at a significant rate, the war chest provides substantial runway to fund the USV division build-out (estimated at $30-40 million), strategic acquisitions, and inventory investments without needing to return to the capital markets in the near term.

The accounts receivable balance of $26.2 million (up from $0.5 million) is worth monitoring closely. While it reflects the rapid scaling of deliveries, it also means the company is extending meaningful credit to defense and government customers. Collection timelines for government contracts can be extended, and this will be a key working capital dynamic to watch.

Manufacturing Scale-Up: The Factory Is the Weapon

Red Cat’s facility expansion from 36,000 to 254,000 square feet represents a 520% increase in manufacturing capacity across four states. The COO’s framing that “the factory is the weapon” is particularly apt in the current defense landscape, where the ability to produce at scale is as strategically important as the technology itself.

Key production milestones include the Salt Lake City facility producing 50 Black Widow drones per day on a single shift, with room to triple lines and add shifts. The FlightWave facility in Torrance is utilizing only one-third of its space to produce 125 Edge 130 drones per month. The Georgia boat factory for Blue Ops went operational in February 2026 with 155,000 square feet and capacity for 100+ USVs per year. This manufacturing infrastructure is not just about meeting current orders it’s about positioning Red Cat to absorb large-scale DoD procurement programs like Drone Dominance, which envisions 350,000 FPV drones.

Earnings Call Takeaways

Blue Ops: Maritime Domain Expansion

The CEO spent considerable time discussing Blue Ops, Red Cat’s maritime USV division launched roughly a year ago. The speed of execution has been impressive: from initial design last August to autonomous boats in the water by December, and a Georgia factory operational by February 2026. The Variant 7 USV integrates both short-range counter-drone capability (ACS Bullfrog, effective to 1,500 yards against FPVs and Shaheds) and long-range capability (Aeon Zeus, 20 km range).

This is strategically significant. Red Cat’s previous drone systems covered approximately 30% of the Earth’s surface; with USVs, the company can now operate across 100% of the globe. The timing is fortuitous given the escalation in the Strait of Hormuz, where USVs offer a compelling alternative to deploying billion-dollar warships for convoy escort missions. The CEO was direct about the opportunity: initial USVs originally planned as demos are now being redirected to customers as quickly as they can be built.

Ukraine: Battlefield Validation

The COO’s report from his trip to Ukraine (he returned the day before the earnings call) was arguably the most impactful segment. Red Cat has established an office in Kyiv, tested multiple systems at the front, and received a Letter of Request from Ukrainian forces to begin replacing Chinese-made ISR drones. The COO shared that Ukrainian forces are consuming approximately 350,000 Chinese ISR drones per year a massive addressable market if Red Cat can capture even a small fraction.

Beyond direct sales, the Ukraine engagement serves as a real-world proving ground. Red Cat has entered into a joint development agreement with a Ukrainian state-owned partner to bring battle-proven technology to its USV platforms. This is reportedly the first such agreement with a non-governmental entity, which could provide significant technology transfer advantages as the company develops next-generation systems.

Drone Dominance: Positioning for the Long Game

Management was candid that Red Cat did not advance past Gauntlet One of the Pentagon’s Drone Dominance competition. However, the CEO framed the broader opportunity compellingly: the program envisions 350,000 FPV drones, which at the typical 20:1 FPV-to-ISR ratio would require approximately 17,500 ISR drones or 8,750 SRR (Short Range Reconnaissance) systems. As the Black Widow is a sensor/ISR platform, Red Cat stands to benefit from the program regardless of the FPV gauntlet outcomes.

Guidance: Deliberately Conservative

Red Cat is not providing formal 2026 guidance at this time, citing the need to have government contracts in hand before committing to numbers. However, the CEO offered an important signal: with Street estimates ranging from $100 million to $170 million for 2026, management indicated they are “very comfortable in the top half” of that range. This implies management confidence in at least $135 million+ in 2026 revenue, which would represent more than 230% growth from FY2025.

The company also committed to updating the market on guidance as soon as contracts are finalized, rather than waiting for the next quarterly call. This approach is prudent given the uncertainty around contract timing during the previous continuing resolution period.

Geopolitical Tailwinds

The timing of the Strait of Hormuz escalation, days after Red Cat’s Innovation Day, has created a surge of inbound interest. The CEO described receiving “panic questions” alongside more structured RFP inquiries from Gulf States and Navy contacts. Counter-drone capability is the most urgent demand area, and Red Cat’s Variant 7 USV with its dual counter-drone configuration is positioned to address this need. The 2026 defense budget plus an additional $150 billion, with potentially another $50 billion related to Iran, represents a dramatically expanded funding environment for exactly the types of systems Red Cat produces.

What I’m Watching Going Forward

Gross Margin Trajectory. The path from 3-4% gross margins to something resembling 20-30%+ is the single most important financial metric for Red Cat over the next 12-18 months. As production scales and fixed cost absorption improves, margins should expand meaningfully. Any quarter that shows material sequential improvement will be a strong signal that the business model is working at scale.

SRR Full Rate Production Contract. The CEO indicated this contract is expected “any day.” Securing the OTA full rate production contract for Black Widow through the SRR program would be the single largest de-risking event for the 2026 revenue outlook and would likely trigger a re-rating.

USV First Deliveries. Management is targeting first USV customer deliveries in 2026. Successful delivery and adoption of USVs would validate the multi-domain strategy and open a new, potentially very large revenue stream.

“That’s it! Thank you very much for reading! You can subscribe and like to support my research and to receive my research right to your inbox. Please make sure to reach out if you have any questions or if you want to chat about markets.”