DraftKings (DKNG) Sniff Test: The Profitability Paradox

Ticker: DKNG | Sector: Consumer Cyclical (Gambling) | Market Cap: ~$11B

I’m introducing a new newsletter the “Sniff Test".

Brett Caughran ex-PM at Citadel and Maverick:

On the Purpose of the Sniff Test

“The goal is to kill the idea before it kills your schedule.”

Opportunity Cost

“If you spend 100 hours on every idea, you will only look at 20 stocks a year. If you can kill an idea in 4 hours, you can cycle through hundreds of names to find the few that truly deserve a deep dive.”

Okay with the explanation out of the way, let’s get into the sniff test of DraftKings

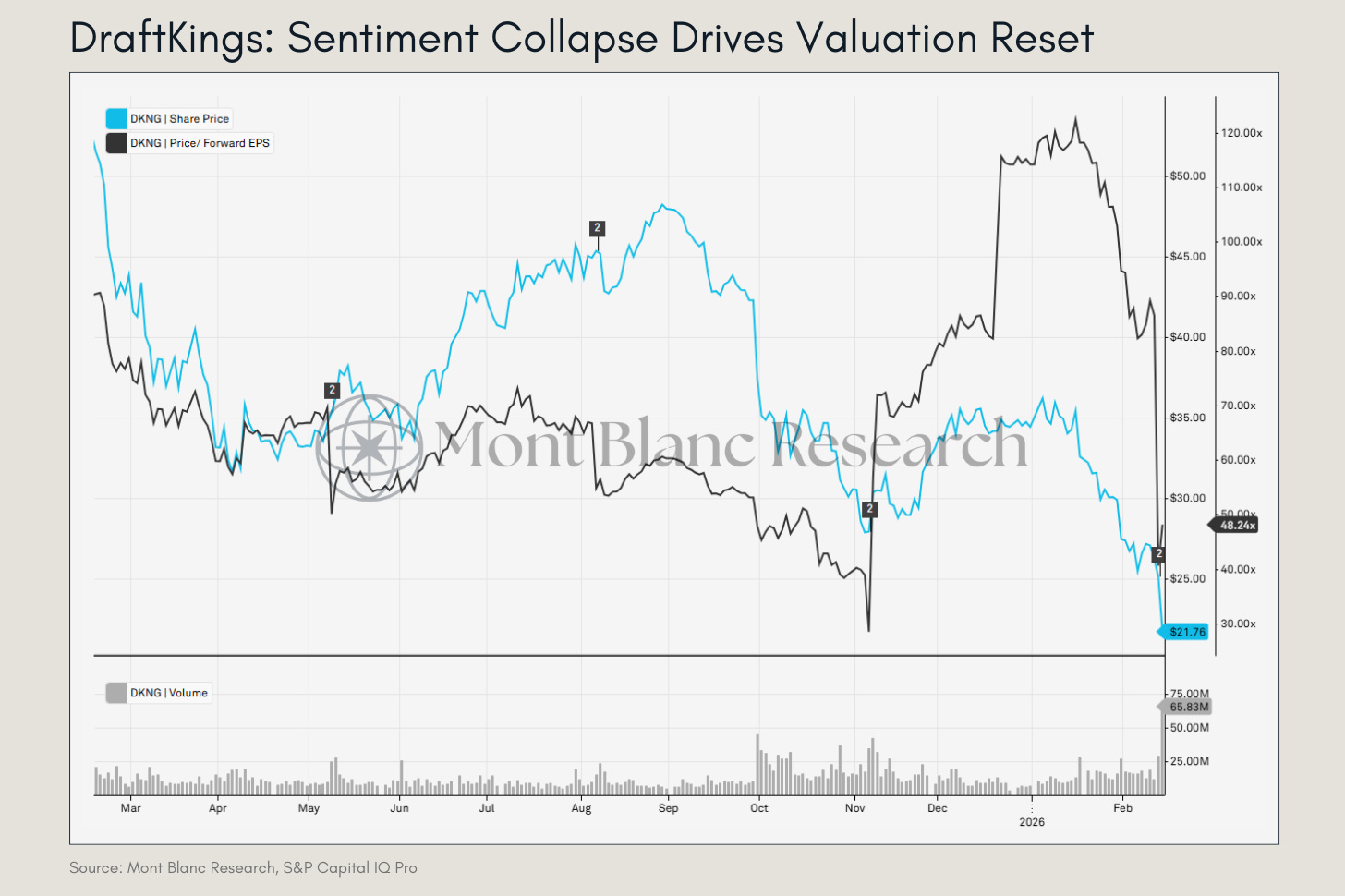

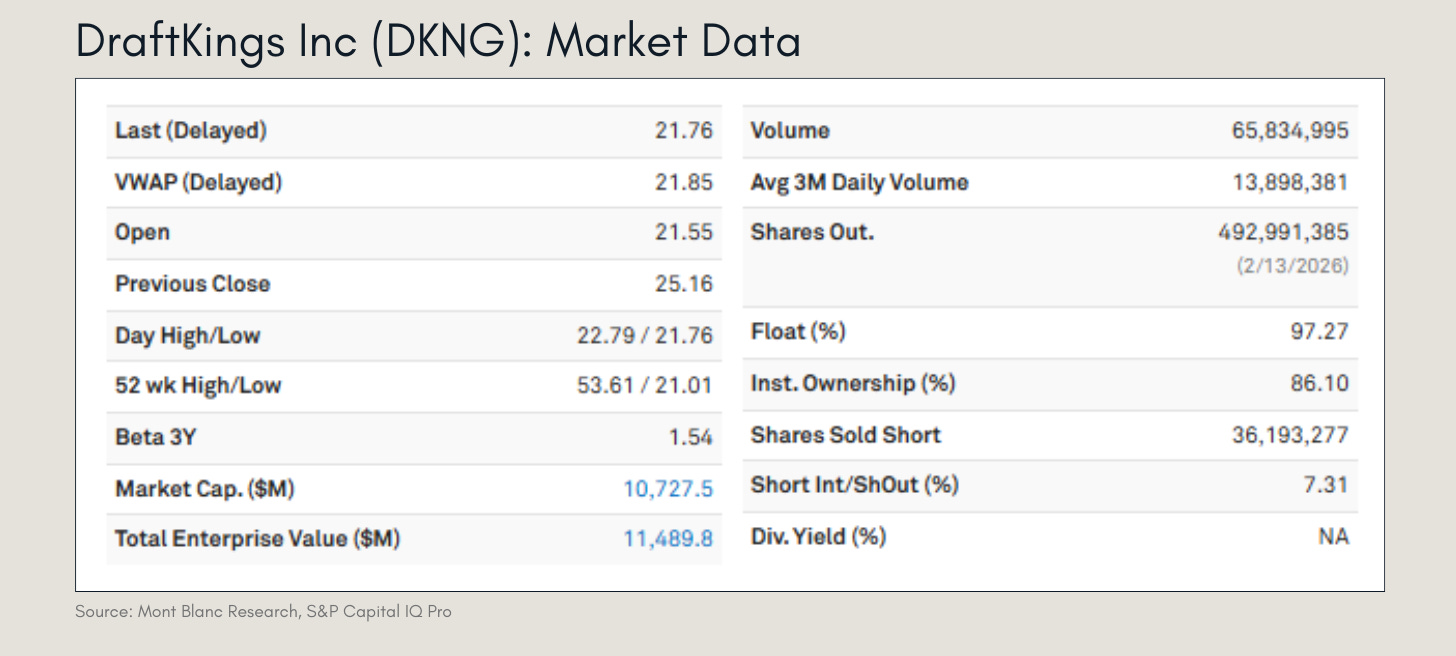

DraftKings Market Data: The Institutional Exit

The immediate “blood test” for DraftKings shows a stock in the middle of a violent institutional re-rating. While the 3-Month Average Daily Volume (ADV) sits at 13.9 million shares, the volume on last Friday was hitting 65.8 million shares.

This 4.7x spike in volume, paired with a 13.5% price collapse, tells us this isn’t a retail flush. Large-scale institutional funds are liquidating positions, and they have more than enough liquidity to do so. At a $10.7 billion Market Cap, DKNG is a deep enough vehicle that funds can exit in size without trapping themselves, which accelerates the downward pressure we’re seeing.

Business Model

DraftKings operates a digital gambling platform that monetises user engagement across sports betting, online casino, and fantasy sports. The core business model is to take a statistical edge on betting activity while increasing customer lifetime value through a multi product ecosystem.

The largest revenue driver is online sportsbook. Users place wagers on sporting events and DraftKings sets odds that embed a house margin. Revenue is determined by total betting volume, known as handle, multiplied by the hold rate. Product innovation such as live betting and same game parlays has structurally increased hold and engagement, making this segment the main growth engine.

The second key pillar is iGaming, which includes online slots, blackjack, and roulette. This is structurally more attractive than sportsbook because margins are higher, outcomes are less volatile, and customer behaviour is more recurring. A major part of the strategy is cross selling sportsbook customers into casino, which significantly increases lifetime value.

The Main Model

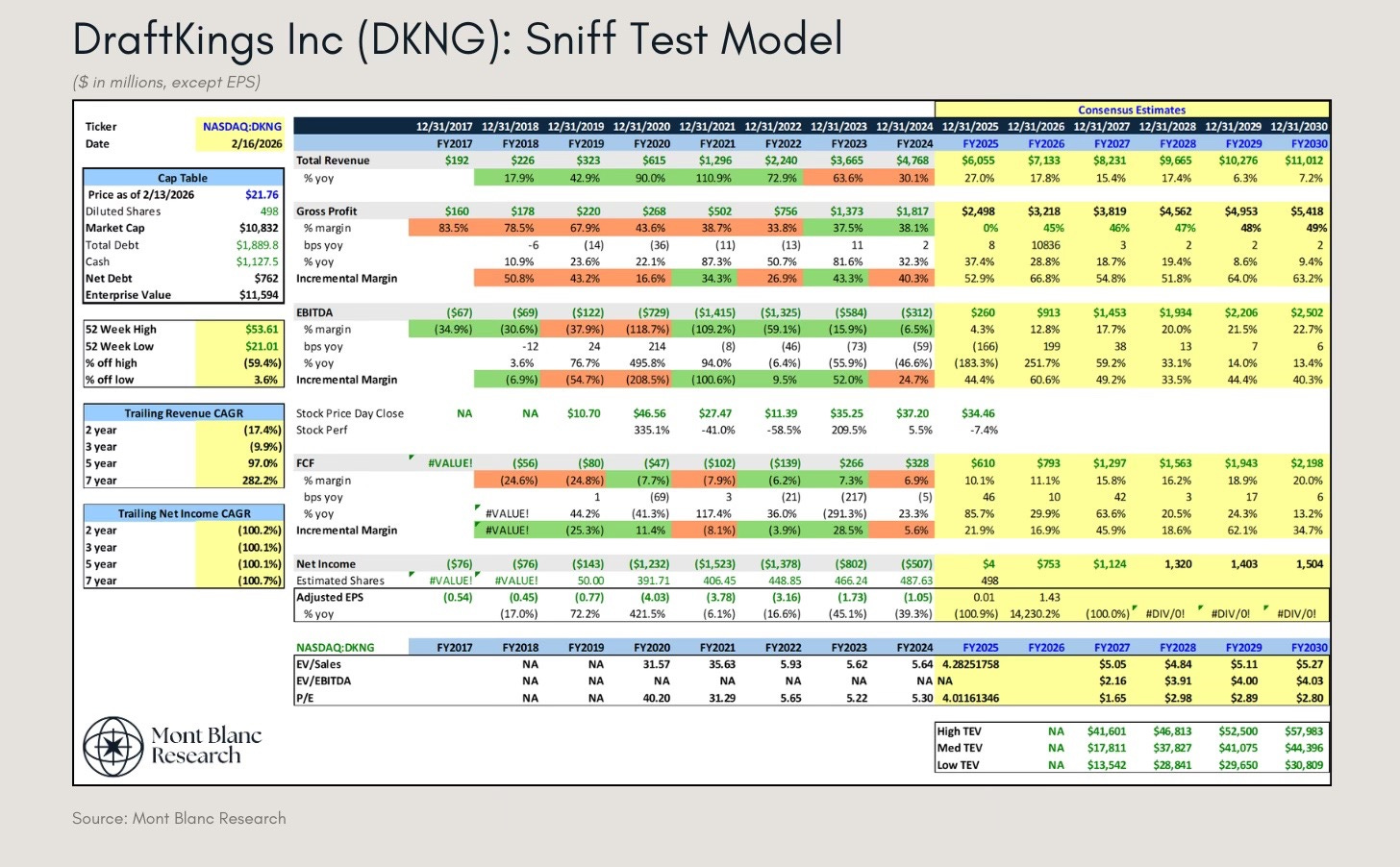

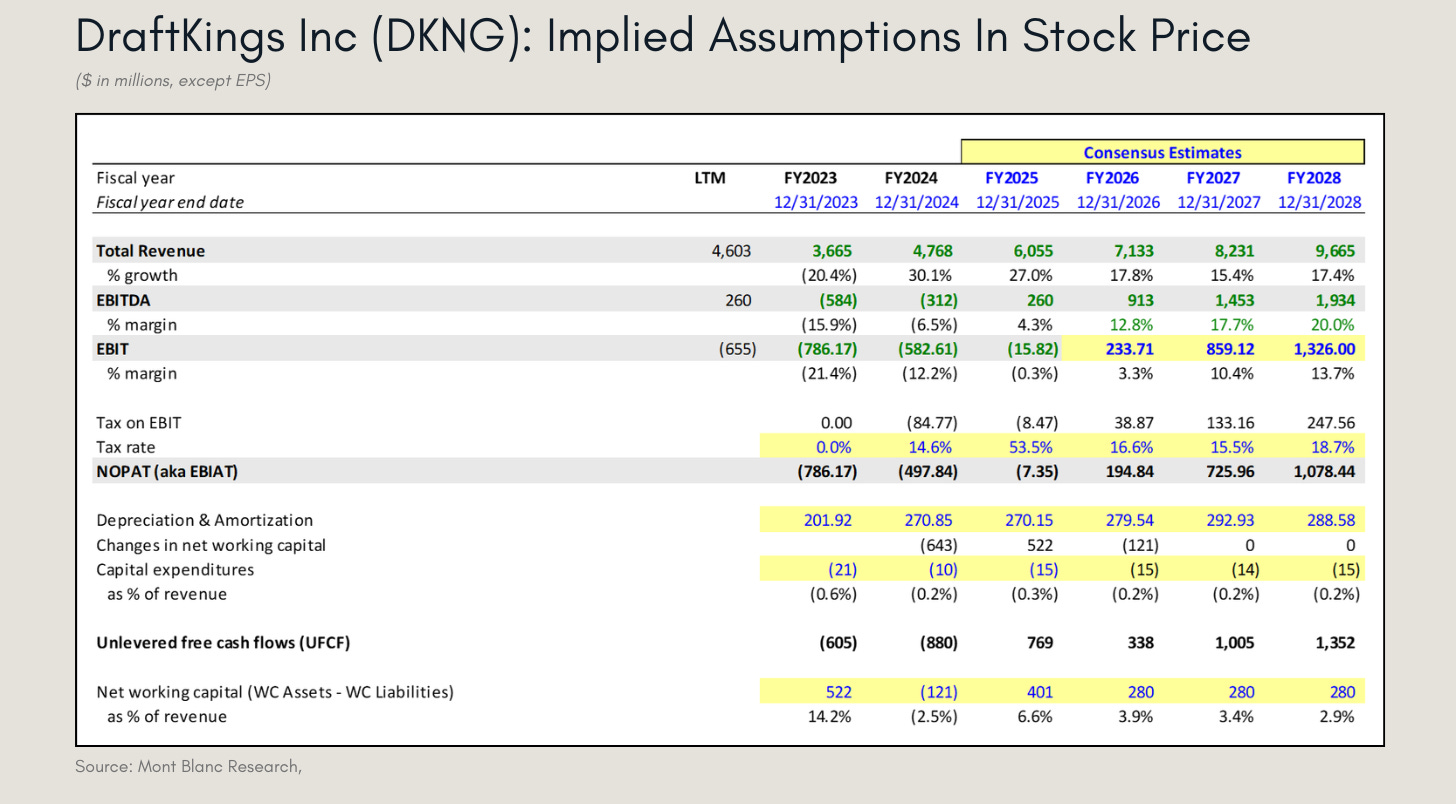

Revenue Growth

Revenue growth over the last nine years has been incredible with annual high double digits growth. Having said that we see that from 2022 onwards there is a deceleration in revenue growth rate. The street estimates suggest this trend will only continue into 2030 where growth is estimated to be 7.2%. This is expected as DraftKings is going though a transition from high growth and not profitable to profitable and high margins. (It’s a rocky transition for DKNG)

According to estimates most of the growth has been organic even though DraftKings has made the acquisitions notably: SBTech in 2020, Diamond Eagle Acquisition Corp 2020 and Golden Nugget Online Gaming (GNOG) 2022.

Margin Trajectory

Margin trajectory is a complicated question for DraftKings. While some metrics are improving other aren’t:

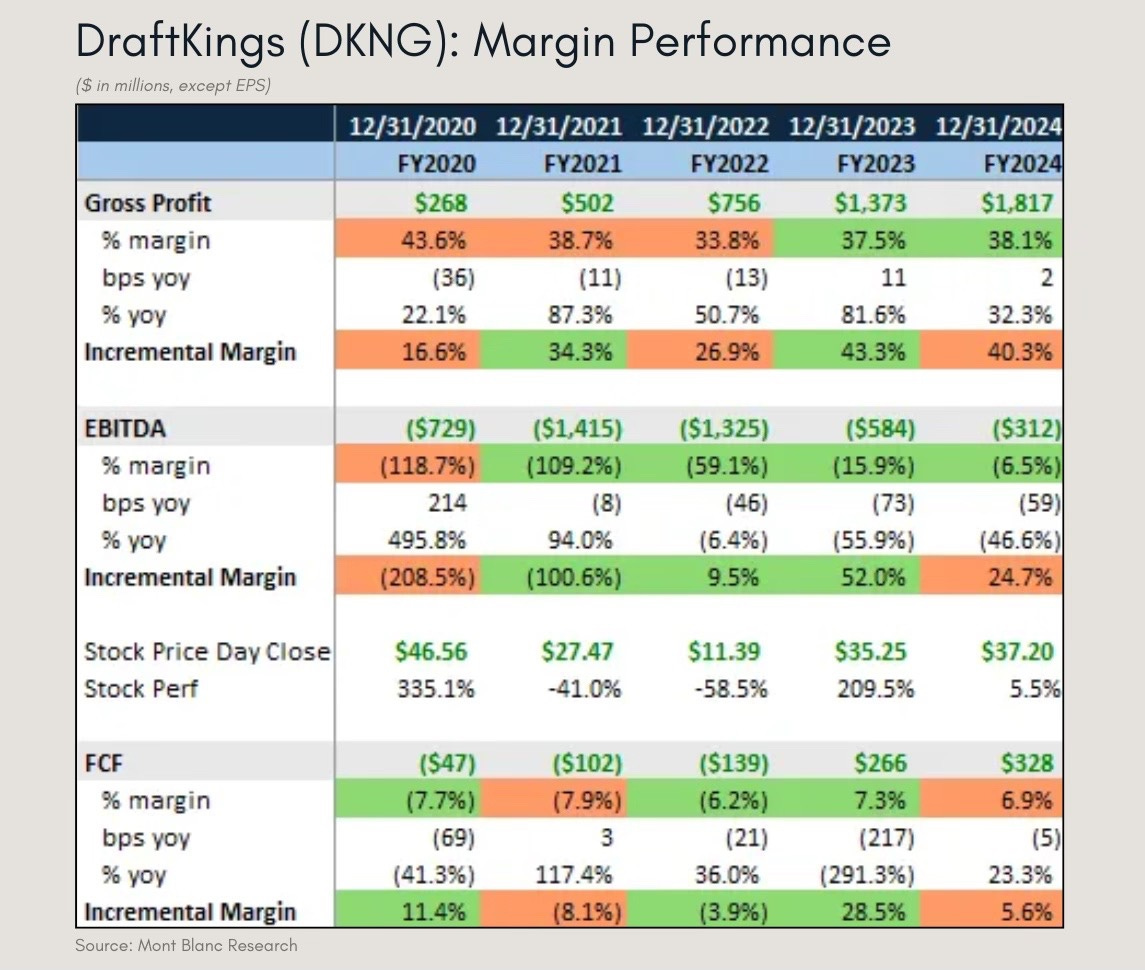

Looking at the last 5 years of margin and incremental margin trajectory. We see gross profit margin improving from FY2022: 3.8% to FY2023: 37.5% to FY2024: 38.1%, at the same time incremental margin has expanded from 26.9% to 40.3%. EBITDA margins have been very consistently improving since 2020, although incremental margin improvement in FY2024 fell to less than half from of previous year to 24.7%. FCF margins were improving until 2023 but took a dive in 2024 especially incremental margin what fell from 28.5 to 5.6%. Margin story overall is mixed.

Valuation and Implied Assumptions

Profitability and Rapid Margin Expansion

The market valuation is currently anchored on a transition from a high-growth, deficit-running operator to a highly efficient cash generator. Specifically, the model assumes that DraftKings will reach a critical profitability inflection point in FY2026 with a double-digit EBITDA margin of 12.8%, eventually scaling to a significant 20% margin by FY2028. For a company that was operating at a -15.9% margin as recently as 2023, this priced-in assumption requires massive operating leverage. It implies that customer acquisition costs (CAC) will fall sharply as the user base matures and the brand moves toward dominance, allowing more of every revenue dollar to flow directly to the bottom line.

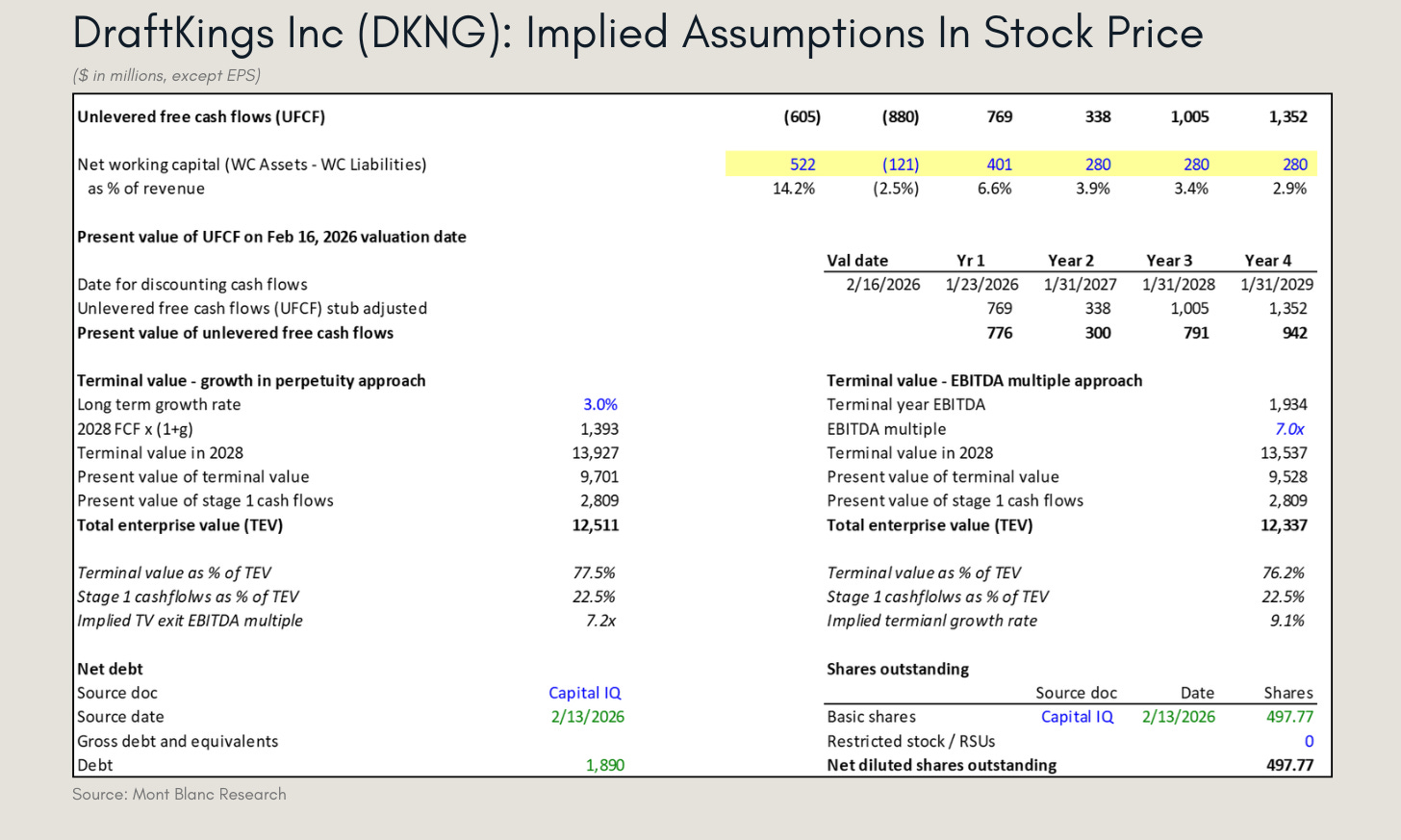

Steady-State Free Cash Flow Requirements

To justify the implied share price of approximately $23.60 (basically where it’s currently trading) the business must generate a steady-state UFCF of $1.35 billion by FY2028. This target is supported by an extremely lean operational assumption: CapEx are projected to remain at just 0.2% of revenue. This suggests that the market views DraftKings as a “capital-light” technology platform rather than a traditional heavy-infrastructure gaming company. Furthermore, Net Working Capital is expected to stabilize at 2.9% of revenue, indicating a highly optimized cash cycle that doesn’t require significant reinvestment to maintain its scale.

Terminal Value and Market Perception

A massive portion of DraftKings’ current value roughly 77.5% of the total Enterprise Value is derived from the Terminal Value (cash flows occurring after 2028). This back-weighted valuation is typical for growth stocks, but it highlights the stock’s sensitivity to long-term growth estimates. The model utilizes a 3.0% long-term growth rate in its assumption.

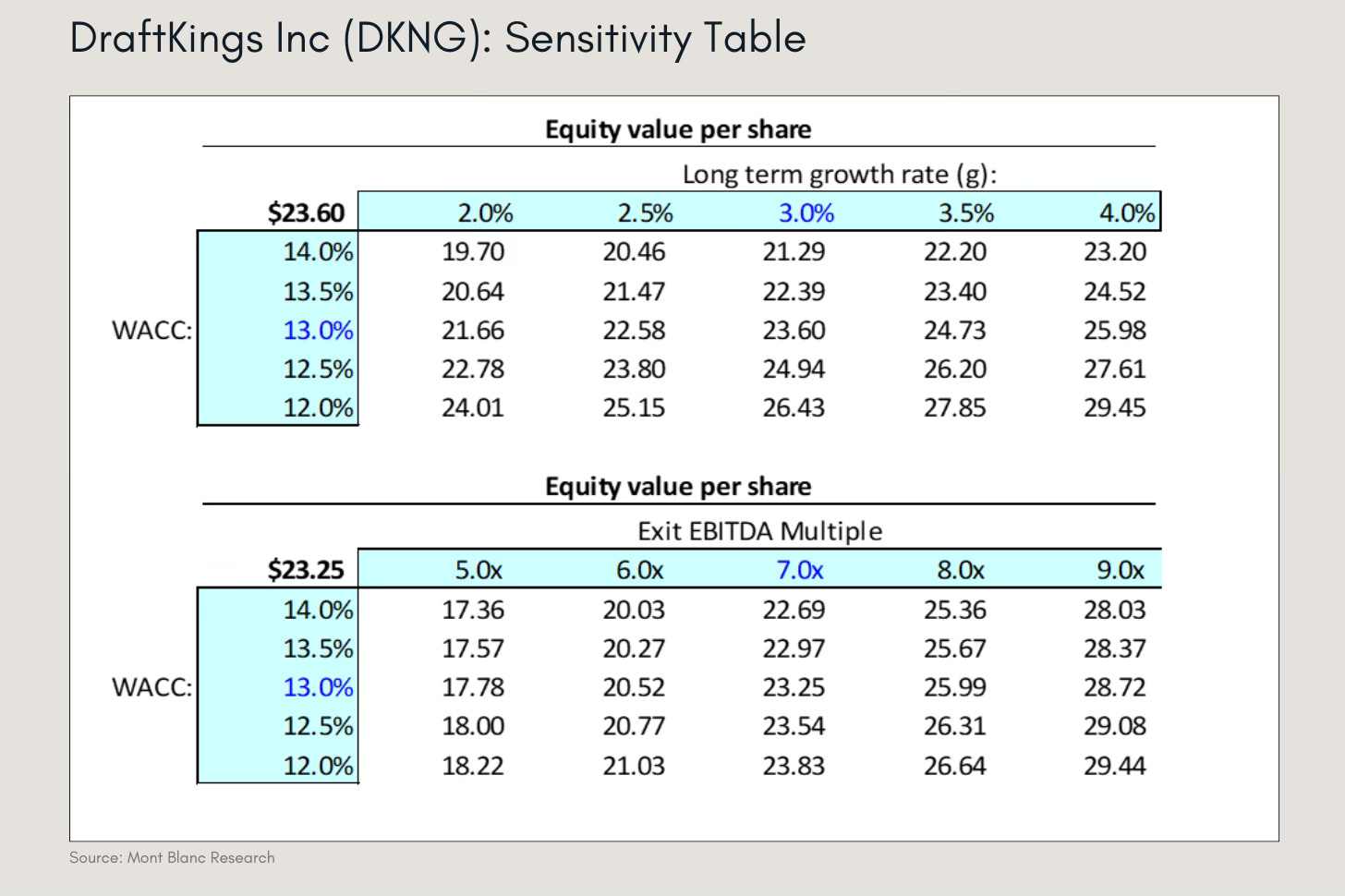

Sensitivity and Valuation Floor

Small shifts in long-term assumptions create significant price swings:

WACC & Growth: At a 13.0% discount rate and 3.0% terminal growth, the value is $23.60. If growth slows to 2.0%, the value falls to $19.70.

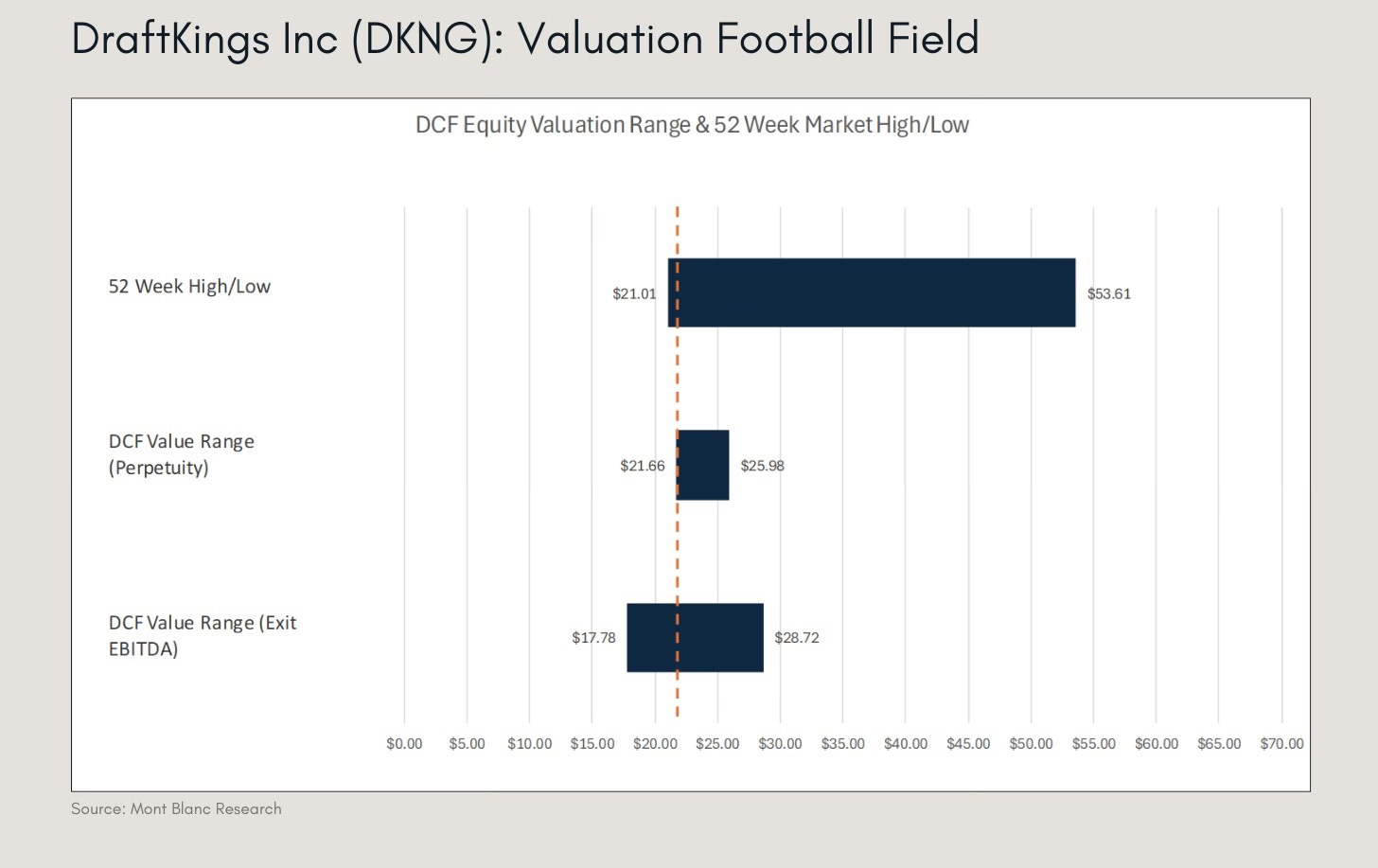

Exit Multiples: The model uses a conservative 7.0x EBITDA multiple to reach $23.25. A more aggressive 9.0x multiple would push the value to $28.72.

Market Position

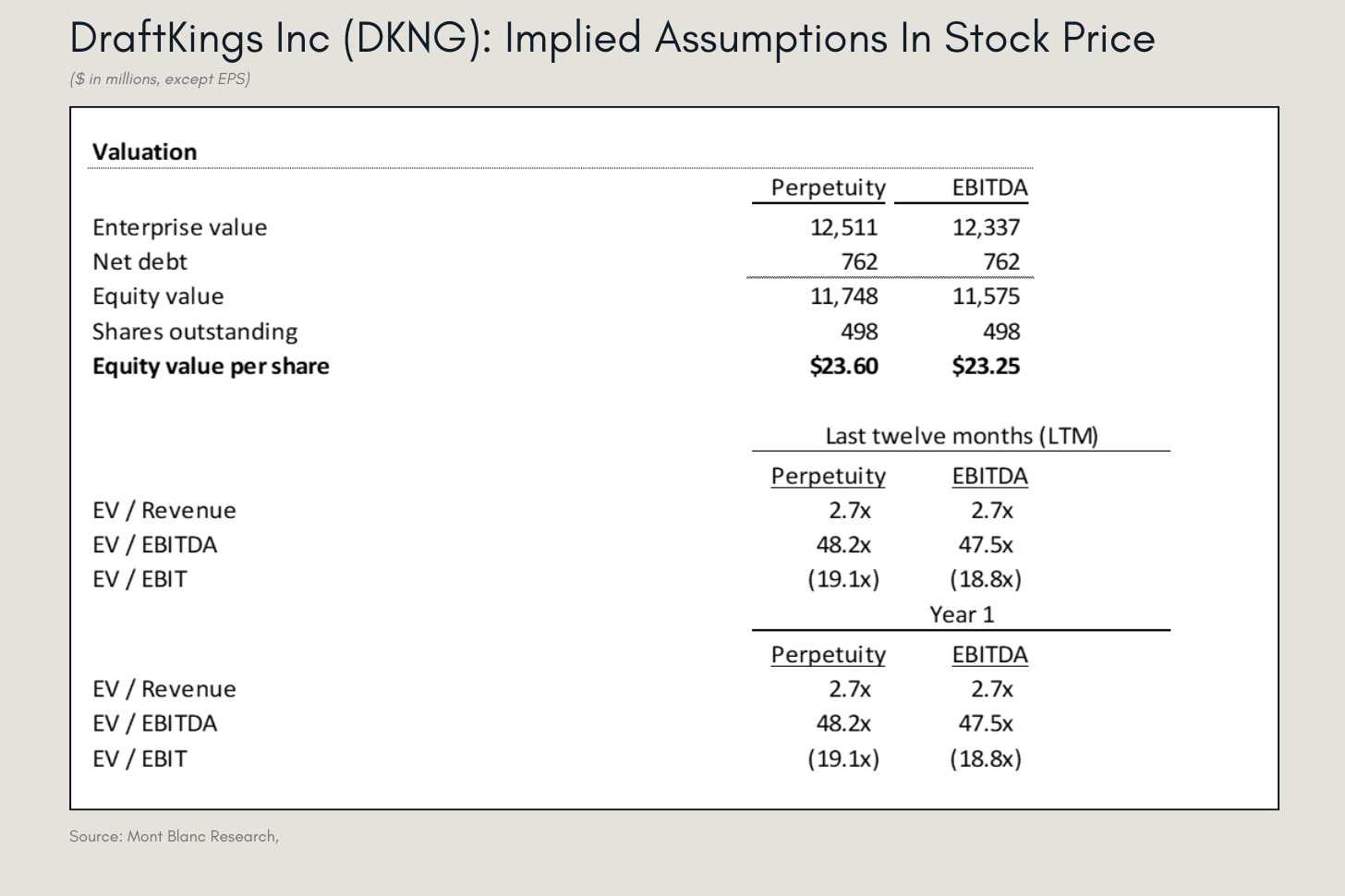

The “Football Field” analysis shows the stock trading near its 52-week low of $21.01, well below its high of $53.61. Current pricing sits at the bottom of the modeled DCF range ($21.66 – $25.98), suggesting the market has stripped away speculative premiums and is now pricing the stock strictly on its ability to hit these 2028 margin targets.

Timeline and Catalysts

Next 6–12 Months: The Execution Catalyst

The most critical event is the Virtual Investor Day (March 2, 2026), where management will likely defend their cautious 2026 guidance and provide a roadmap for Winning in Predictions. Over the next year, the full integration of Railbird Technologies will be essential for technical efficiency. Investors will also be hyper-focused on any state-level tax adjustments (like those in Illinois) and how the company uses its cash active share buybacks at these $21–$23 levels would serve as a powerful signal that management believes the stock is fundamentally undervalued.

Next Quarter: The Sanity Check

Next quarter, the Football Field chart will be put to the test as investors look at Monthly Unique Player (MUP) growth to see if it has truly plateaued. To support the modeled $23.60 fair value, the company must demonstrate an improving hold rate (the percentage of bets the house keeps) and show that marketing costs are finally shrinking as a percentage of revenue. Any beat on these operational metrics could quickly push the stock from its current floor toward the upper end of the valuation range.

Key Risks

Growth Stagnation The “MUP” Problem

Monthly Unique Payers (MUPs) have stalled at 4.8 million, suggesting the platform may be reaching a ceiling in existing markets. If DraftKings cannot reignite user growth, reaching the projected $9.6 billion revenue target for 2028 becomes entirely dependent on squeezing more money out of a fixed user base a difficult strategy in a competitive market.

2. Guidance Credibility & Margin Compression

Management’s recent 8% revenue guidance miss for 2026 has created a credibility gap. Compounding this are state tax hikes, like those in Illinois, which directly eat into the bottom line. If more states follow suit, the goal of a 20% EBITDA margin could shift from a base-case assumption to an unattainable best-case scenario.

3. High-Stakes Competition in Predictions

The pivot into Prediction Markets is meant to be a $10 billion growth engine, but it pits DraftKings against deep-pocketed tech rivals like Robinhood and Coinbase. Unlike sportsbooks, these rivals have massive, existing user bases and could trigger a new marketing war that forces DraftKings to spend heavily, delaying their timeline for consistent free cash flow.

Verdict: WATCHLIST

DraftKings has shifted from a growth at all costs story to a high-stakes execution play, trading near its 52-week low of $21.01. The market is skeptical of management’s conservative 2026 guidance and stalling user growth.

DraftKings is a bet on whether a dominant sportsbook can successfully pivot into high-margin prediction markets to hit a 20% EBITDA margin by 2028. Even though the the stock is trading near its 52-week low of $21.01, I’d wait to see margin trajectory improvements into the next quarter to start thinking about investing.

What Would Change My Mind

Regulatory Dominoes: If more states follow Illinois in tripling gambling taxes, the 20% margin target becomes mathematically impossible.

Platform Fatigue: Evidence that users are shifting money into Predictions rather than adding new funds (cannibalization).

Competitive Re-acceleration: If marketing spend must stay high to fight off FanDuel or Robinhood, the lean cash flow thesis breaks.

“That’s it! Thank you very much for reading! You can subscribe and like to support my research and to receive my research right to your inbox. Please make sure to reach out if you have any questions or if you want to chat about markets.”

Interesting how much of the valuation sits in the terminal year. 77% of the enterprise value coming from cash flows after 2028 means the near-term execution matters less for the math than the long-term assumptions. That kind of structure tends to make stocks sensitive to any news that shifts people's view of what that endpoint looks like.